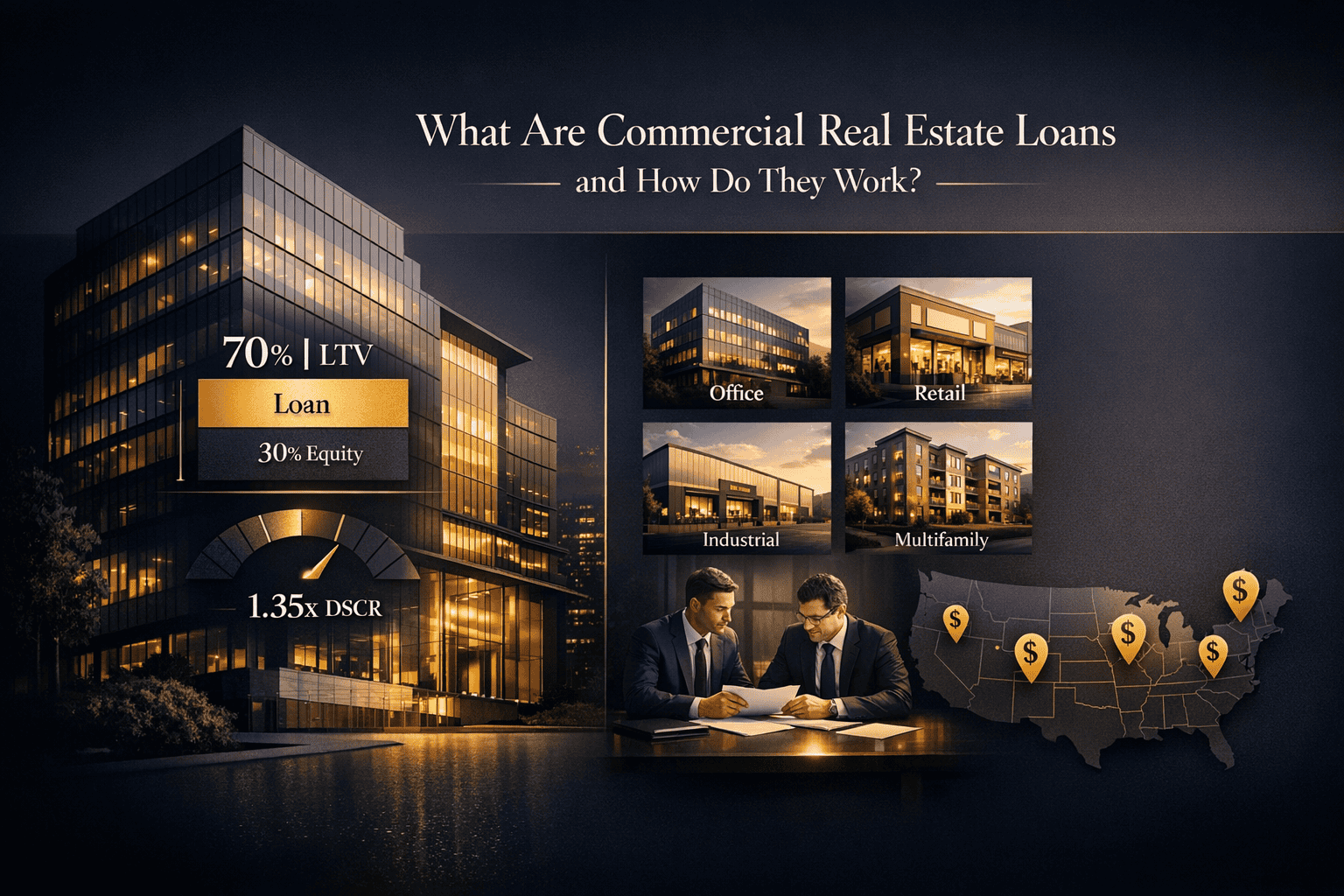

What Are Commercial Real Estate Loans?

Commercial real estate loans are financing instruments used to purchase, refinance, or develop income-producing properties. Unlike residential mortgages, which are designed for personal homes, commercial real estate loans are structured around properties that generate revenue — such as office buildings, retail centers, multifamily apartment complexes, industrial warehouses, and mixed-use developments.

At Cordura, we work with investors and buyers across the US market who rely on these loans to fund significant real estate transactions. Understanding how they work is the first step toward making smarter investment decisions.

How Do Commercial Real Estate Loans Work?

Commercial real estate loans function similarly to residential mortgages in some ways — a lender provides capital, and the borrower repays the loan with interest over time. However, the underwriting criteria, loan structures, and terms are considerably different.

Key Factors Lenders Evaluate

- Debt Service Coverage Ratio (DSCR): Lenders assess whether the property's net operating income (NOI) is sufficient to cover loan payments. A DSCR of 1.25 or higher is typically required.

- Loan-to-Value Ratio (LTV): Most commercial loans cap at 65%–80% LTV, meaning borrowers must bring a significant down payment.

- Borrower Creditworthiness: Both personal credit scores and business financials are reviewed.

- Property Type and Condition: The asset class, location, and physical condition all influence approval and terms.

- Business Plan: Especially for development or value-add deals, lenders want to see a credible exit strategy.

Types of Commercial Real Estate Loans

There is no single loan product that fits every commercial deal. Below are the most common types available to investors and buyers in the US market.

1. Traditional Commercial Mortgages

Offered by banks and credit unions, these are long-term loans — typically 5 to 20 years — with amortization periods of up to 30 years. They often carry competitive interest rates and are best suited for stabilized, income-producing properties.

2. SBA 7(a) and SBA 504 Loans

The U.S. Small Business Administration backs these loan programs for owner-occupied commercial properties. SBA 504 loans are particularly popular for purchasing real estate because they allow down payments as low as 10%, making them accessible for small business owners.

3. CMBS Loans (Commercial Mortgage-Backed Securities)

These loans are pooled together and sold to investors as securities. CMBS loans typically offer fixed rates and non-recourse terms, meaning the borrower's personal assets are not at risk if the loan defaults. They are best for larger, stabilized assets.

4. Bridge Loans

Bridge loans are short-term financing solutions — usually 6 to 36 months — designed to bridge the gap between acquiring a property and securing long-term financing. They are ideal for value-add projects or properties transitioning between tenants. If you're exploring active investment opportunities, our commercial real estate listings include properties suited for bridge financing strategies.

5. Hard Money Loans

Provided by private lenders, hard money loans are asset-based, meaning approval relies heavily on the property's value rather than the borrower's credit. They carry higher interest rates (8%–15%) and short terms, making them suitable for quick acquisitions or fix-and-flip commercial projects.

6. Construction Loans

These fund the ground-up development of commercial properties. Funds are released in draw schedules as construction milestones are met. Upon completion, borrowers typically refinance into a permanent loan.

Commercial Loan Terms and Structure

Understanding the structure of a commercial real estate loan helps borrowers negotiate better deals and avoid costly surprises.

Amortization vs. Loan Term

A common feature of commercial loans is the balloon payment. For example, a loan may have a 25-year amortization schedule but a 10-year term, meaning the remaining balance is due as a lump sum at the end of year 10. Borrowers must plan to refinance or sell before the balloon date.

Interest Rates

Commercial loan rates can be fixed or variable. Fixed rates offer payment predictability, while variable rates — often tied to SOFR or Prime Rate — may start lower but carry more risk over time. As of 2024, commercial mortgage rates typically range from 6% to 10%, depending on the loan type, property, and borrower profile.

Prepayment Penalties

Many commercial loans include prepayment restrictions such as step-down penalties, yield maintenance, or defeasance clauses. These protect lenders from early repayment and must be factored into exit strategy planning.

The Commercial Loan Application Process

Securing a commercial real estate loan requires thorough preparation. Here's what the typical process looks like:

- Step 1 – Identify the Property: Before approaching lenders, have a specific property in mind with a clear business case.

- Step 2 – Gather Documentation: Lenders will request rent rolls, operating statements, tax returns, personal financial statements, and property appraisals.

- Step 3 – Submit a Loan Application: Provide all required documentation along with your business plan or pro forma projections.

- Step 4 – Underwriting: The lender evaluates the property, borrower, and market. This can take 30 to 60 days or more.

- Step 5 – Term Sheet and Commitment: If approved, a term sheet outlining loan terms is issued. Review this carefully before signing.

- Step 6 – Closing: Final legal documents are signed, funds are disbursed, and the transaction closes.

Commercial Loans vs. Residential Mortgages

It's important to understand the distinct differences between these two financing categories before entering the market.

- Loan Purpose: Residential loans fund personal homes; commercial loans fund income-generating assets.

- Down Payments: Commercial loans typically require 20%–35% down versus 3%–20% for residential.

- Approval Criteria: Commercial underwriting focuses heavily on the property's income and the borrower's business strength.

- Loan Terms: Shorter terms with balloon payments are common in commercial lending.

- Interest Rates: Commercial rates are generally higher due to perceived risk.

If you're still exploring whether commercial property is the right investment for you, our guide on why investing in commercial real estate can help you evaluate the potential returns and risks involved.

Who Qualifies for a Commercial Real Estate Loan?

Qualification standards vary by lender and loan type, but generally, the strongest borrowers share these characteristics:

- A credit score of 680 or higher (some lenders require 700+)

- Sufficient liquidity to cover down payment and reserves

- Experience owning or managing commercial properties

- A well-performing property with strong NOI and occupancy rates

- A detailed business plan or investment strategy

First-time investors are not excluded, but they may face stricter terms or need to partner with more experienced sponsors to secure financing.

Tips for Getting the Best Commercial Real Estate Loan

- Shop multiple lenders: Banks, credit unions, insurance companies, and private lenders all offer different products. Comparing options can save significant money over the life of a loan.

- Work with a commercial mortgage broker: A broker can connect you with a wide network of lenders and negotiate on your behalf.

- Improve your DSCR: Increasing the property's income before applying strengthens your application considerably.

- Understand your exit strategy: Know whether you plan to sell, refinance, or hold — and choose loan terms that align with that strategy.

- Hire experienced legal counsel: Commercial loan documents are complex. An attorney familiar with real estate finance can help you avoid unfavorable clauses.

How Cordura Supports Commercial Real Estate Investors

Whether you're acquiring your first income property or expanding a diversified portfolio, Cordura provides the market intelligence and property access you need to execute with confidence. Our team serves investors, buyers, and property seekers across the US market, helping match the right opportunities with the right capital strategies.

Ready to find your next investment? Explore our curated commercial real estate listings and take the first step toward building long-term wealth through commercial property ownership.

Final Thoughts

Commercial real estate loans are powerful tools for building wealth through property — but they come with complexity that demands careful planning. By understanding loan types, underwriting criteria, and structural nuances, investors can approach lenders with confidence and secure financing that aligns with their long-term goals. As the market continues to evolve, staying informed is your most valuable competitive advantage.