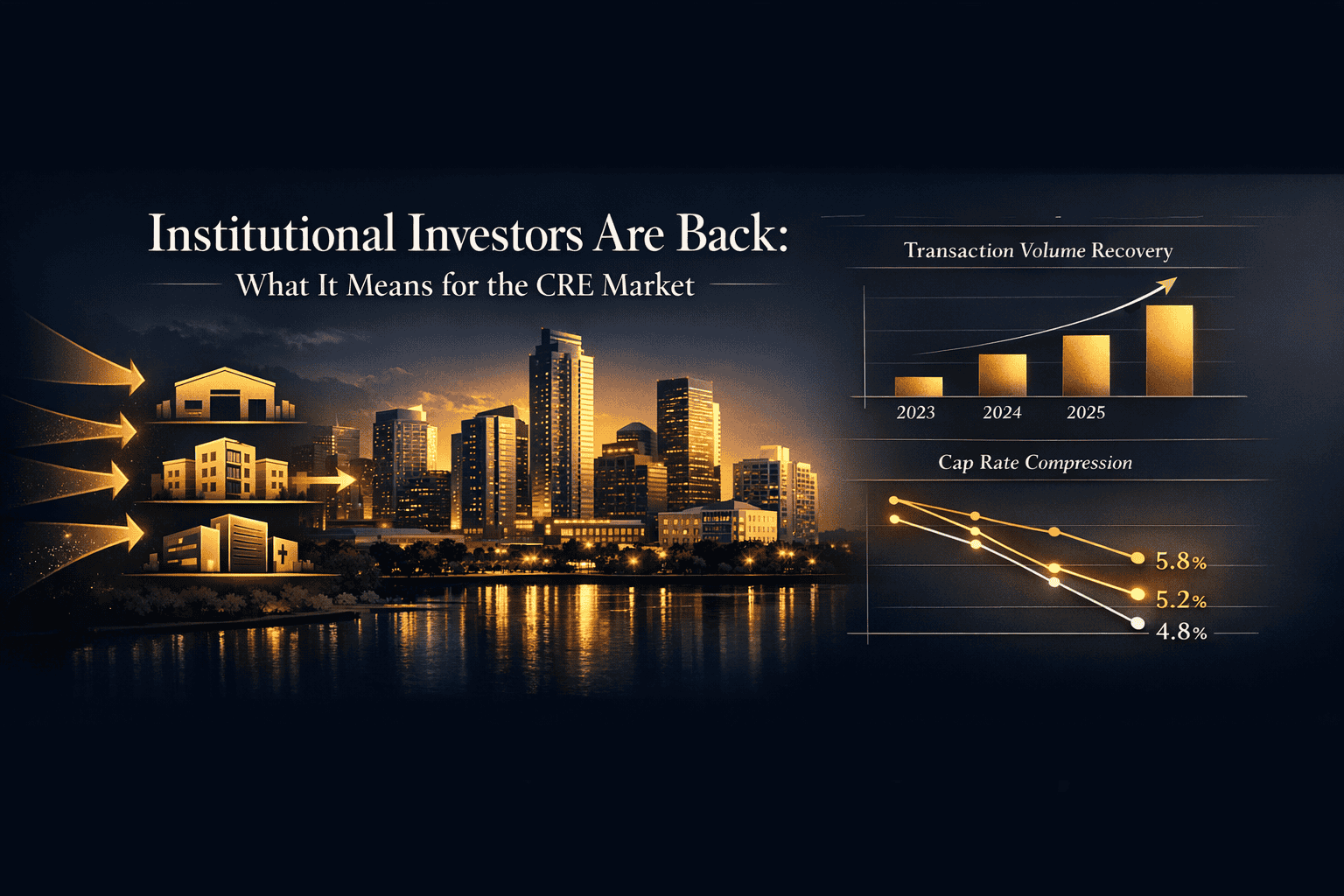

Institutional Investors Are Back: What It Means for the CRE Market

After a period of cautious retreat, institutional investors are returning to commercial real estate with renewed confidence. Rising interest rates, inflation uncertainty, and valuation corrections kept major capital allocators on the sidelines throughout much of 2022 and 2023. But the landscape has shifted. Stabilizing rates, improving fundamentals in select asset classes, and repriced valuations have created a compelling re-entry window — and institutional money is moving fast.

For individual investors, buyers, and property seekers, understanding what this capital surge means for the market is critical. Institutional activity reshapes pricing, competition, and deal flow across nearly every CRE sector. At Cordura, we track these macro shifts closely to help our clients stay ahead of the curve.

Why Institutional Capital Pulled Back — And Why It's Returning

To understand the current resurgence, it helps to revisit why institutional investors stepped back in the first place. The Federal Reserve's aggressive rate hike cycle between 2022 and 2023 triggered a dramatic repricing event across commercial real estate. Cap rates expanded, transaction volumes plummeted, and many institutional players — pension funds, REITs, sovereign wealth funds, and private equity real estate firms — chose to pause deployment while waiting for price discovery.

By late 2024 and into 2025, several key conditions realigned:

- Interest rate stabilization: The Fed's pivot toward rate cuts signaled a more predictable financing environment, making long-term underwriting more reliable.

- Valuation resets: Many CRE assets have repriced significantly from their 2021 peaks, offering institutional buyers better entry points and improved return potential.

- Dry powder pressure: Institutional funds raised billions in capital commitments during 2021–2022. Sitting on uninvested capital too long creates performance drag — investors are now compelled to deploy.

- Sector-specific resilience: Industrial, multifamily, data centers, and healthcare real estate have demonstrated durable demand fundamentals, attracting fresh institutional interest.

Which CRE Sectors Are Attracting the Most Institutional Capital?

Industrial and Logistics

Industrial real estate remains a top institutional target. E-commerce growth, supply chain reshoring, and last-mile delivery infrastructure needs continue to drive demand for warehouse and distribution space. Vacancy rates in prime industrial markets remain low, and rental growth — while moderating — still outpaces historical averages. Institutions are acquiring both stabilized assets and development sites, particularly in Sun Belt markets and major port-adjacent metros.

Multifamily

Despite elevated construction deliveries in some markets, multifamily housing fundamentals remain strong across much of the US. The structural undersupply of housing, rising homeownership costs, and demographic tailwinds from millennials and Gen Z renters continue to support institutional demand for apartment assets. Value-add plays in secondary markets have become particularly attractive as primary coastal markets face supply headwinds.

Data Centers and Digital Infrastructure

Perhaps the most dramatic institutional capital surge is targeting data centers and digital infrastructure. The artificial intelligence boom has created an insatiable appetite for computing power, and data center demand is outpacing new supply in virtually every major hub. Institutional investors — including global sovereign wealth funds and major REITs — are committing billions to this sector, often through joint ventures with established operators.

Healthcare and Life Sciences

Medical office buildings, senior housing, and life sciences facilities are drawing institutional attention as aging demographics and biotech growth create durable demand drivers. These assets offer attractive yield spreads and long-term lease structures that align well with the investment horizons of pension funds and insurance companies.

Office: A Selective Recovery

Office remains the most nuanced story. Blanket institutional avoidance of office is giving way to selective acquisition of trophy and Class A assets in high-demand urban cores. While suburban and commodity office continues to struggle, best-in-class office space in cities like New York, Boston, and Miami is attracting interest from value-oriented institutional buyers who see deep discounts relative to replacement cost.

How Institutional Re-Entry Affects Pricing and Competition

The return of institutional capital has direct implications for pricing dynamics across CRE asset classes. When large pools of capital compete for a limited supply of quality assets, cap rates compress and seller leverage increases. Markets that were heavily buyer-friendly through 2023 are beginning to tighten again in sectors where institutional demand is concentrating.

For private investors and smaller buyers, this creates both challenges and opportunities:

- Increased competition on core assets: Institutional buyers will aggressively pursue stabilized, income-producing properties in primary markets, making it harder for smaller investors to win deals on price alone.

- Opportunity in overlooked segments: Institutions typically focus on larger deal sizes and primary markets. Secondary and tertiary markets, as well as smaller asset sizes, remain less competitive — a potential advantage for individual investors.

- Rising valuations lift all boats: As institutional capital drives up prices in core sectors, the valuation uplift can benefit existing owners across adjacent asset classes and markets.

- JV and co-investment opportunities: Some institutional platforms actively seek local operating partners and co-investors for value-add and development deals — creating partnership pathways for private capital.

If you're actively evaluating acquisition opportunities, our CRE investment insights can help you understand where pricing is moving and which markets offer the best risk-adjusted returns right now.

Geographic Markets Seeing the Strongest Institutional Activity

Institutional capital is not flowing uniformly across the US. Certain markets are capturing a disproportionate share of investment activity based on population growth, infrastructure investment, and business climate.

Sun Belt Dominance

Markets like Dallas-Fort Worth, Phoenix, Nashville, Atlanta, and Charlotte continue to attract outsized institutional attention. Strong population inflows, business-friendly regulatory environments, and relatively lower land costs make these metros compelling for both industrial and multifamily investment.

Gateway City Selective Recovery

New York, Los Angeles, Boston, and Chicago are seeing selective institutional re-entry, particularly in multifamily and premium office. These markets offer liquidity and depth that smaller metros cannot match, making them attractive for large capital pools that need to deploy at scale.

Emerging Tech and Logistics Hubs

Secondary markets with strong tech employment bases — Austin, Denver, Raleigh-Durham, and Salt Lake City — are attracting institutional interest in both office and industrial assets as employers diversify their footprints beyond traditional gateway cities.

What Individual Investors and Property Buyers Should Do Now

The return of institutional capital is a market signal that demands attention. Whether you're a seasoned investor, a first-time commercial property buyer, or a business owner evaluating your real estate strategy, here's how to position yourself effectively:

- Move decisively on quality assets: The window for buying repriced assets before institutional capital fully normalizes valuations is narrowing. Extended deliberation in a competitive rebound environment can be costly.

- Focus on sectors with durable fundamentals: Align your investment thesis with the sectors institutional capital is validating — industrial, multifamily, healthcare — rather than swimming against structural headwinds.

- Leverage local market intelligence: Institutional buyers operate at scale but often lack the local market depth that regional specialists possess. This knowledge gap is your competitive advantage.

- Consider the full capital stack: With institutional equity re-entering the market, debt markets are also loosening. Evaluate creative financing structures including CMBS, agency debt, and bridge loans to optimize your capital stack.

- Partner with experienced advisors: In a market where conditions are shifting rapidly, having the right advisory team can mean the difference between winning and losing deals.

At Cordura, we work with investors at every stage of the acquisition and disposition process. Connect with our team to discuss how the current institutional re-entry cycle creates opportunities specific to your investment goals and target markets.

The Broader Economic Signal: What Institutional Confidence Tells Us

Institutional investors are among the most sophisticated capital allocators in the world. Their return to CRE is not a casual or reactive decision — it represents months of rigorous underwriting, macroeconomic analysis, and risk assessment. When pension funds, sovereign wealth funds, and major private equity platforms simultaneously re-enter a market, it sends a powerful signal: the fundamental value proposition of commercial real estate remains intact, and the risk-reward calculus has shifted favorably.

This does not mean the market is without risk. Interest rate volatility, geopolitical uncertainty, and sector-specific oversupply in some markets remain real considerations. But the directional signal from institutional capital is clear — commercial real estate is entering a new cycle, and early movers stand to benefit most.

Final Thoughts: Positioning for the New CRE Cycle

The institutional re-entry into commercial real estate marks the beginning of a meaningful market recovery cycle. For investors and buyers who have been waiting for clearer signals, the institutions have effectively fired the starting gun. The question now is not whether to engage with the market — it's how to do so strategically, with a clear understanding of sector dynamics, geographic trends, and competitive positioning.

Cordura is committed to providing our clients with the market intelligence, deal access, and advisory expertise needed to navigate this evolving landscape with confidence. Whether you're evaluating your first commercial acquisition or managing a diversified portfolio, the current environment rewards preparation, conviction, and the right partnerships.