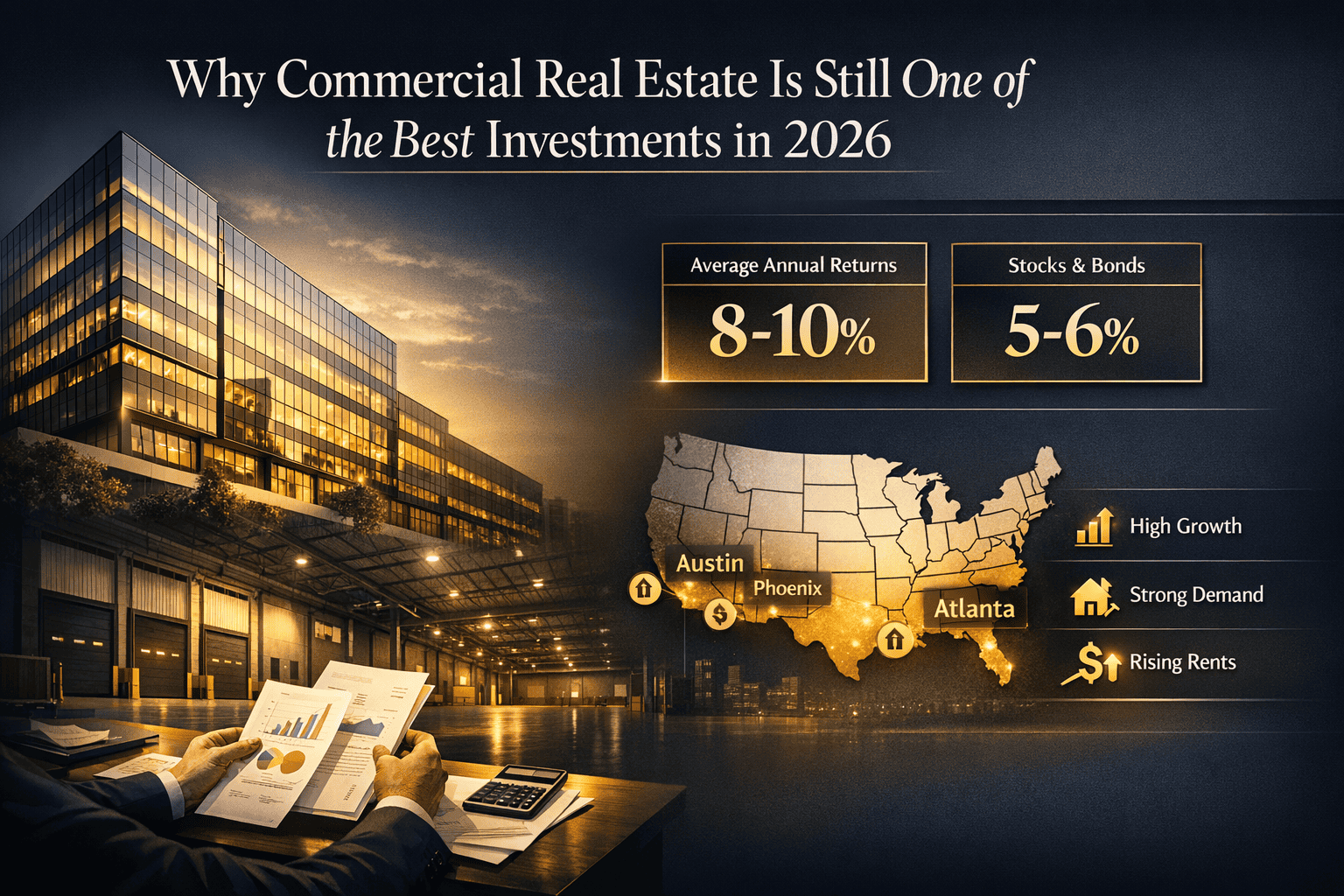

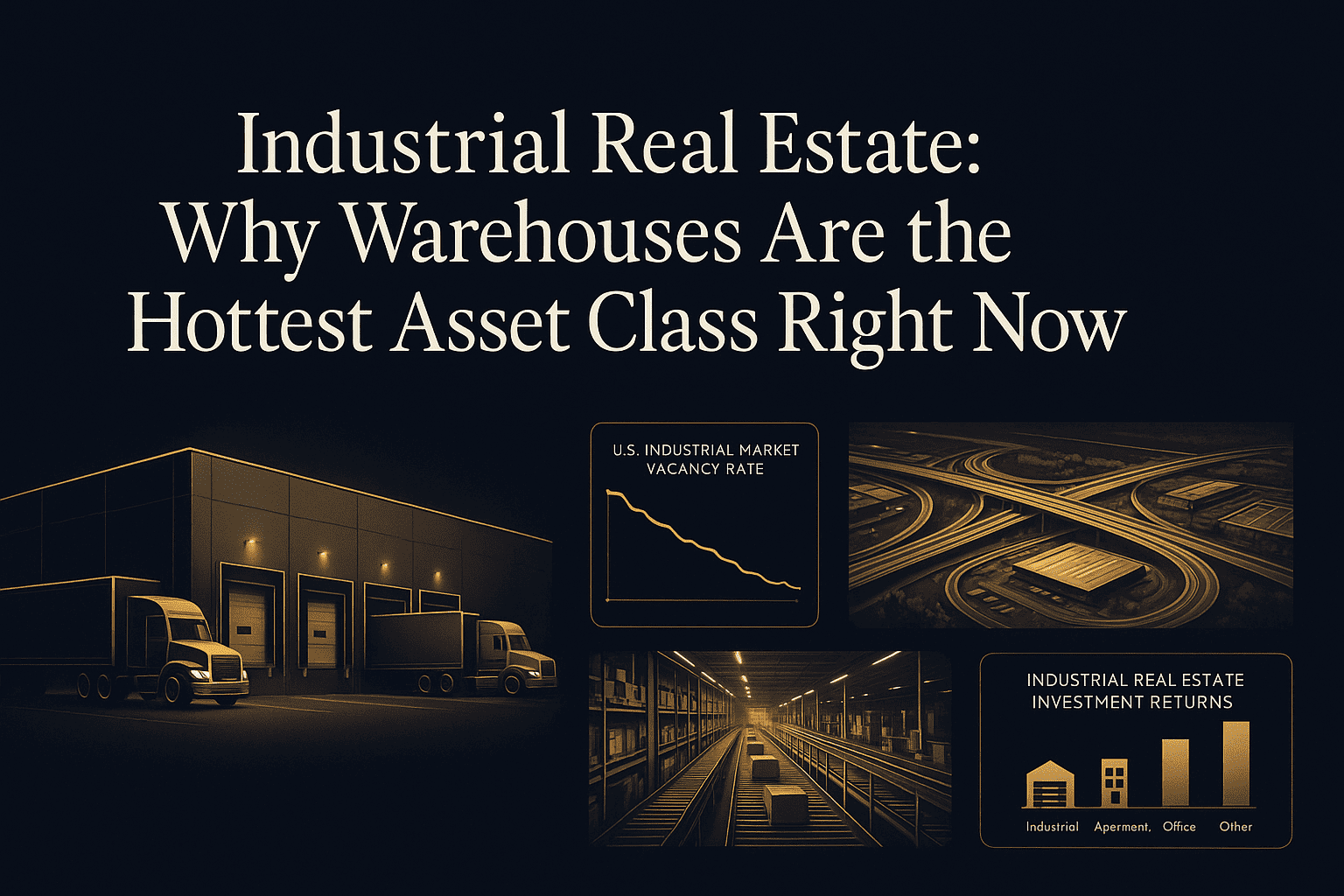

Industrial Real Estate: Why Warehouses Are the Hottest Asset Class Right Now

If you've been watching the commercial real estate landscape over the past few years, one trend stands out above the rest: industrial real estate — and warehouses in particular — has become the undisputed darling of the investment world. Cap rates are compressing, vacancy rates are near historic lows, and institutional capital is flooding in at record pace. Whether you're a seasoned investor or just beginning to explore commercial real estate investment, understanding why warehouses are dominating the market right now is essential to making smart, forward-thinking decisions.

The E-Commerce Revolution and Its Lasting Impact

The seismic shift toward online shopping didn't just change how consumers buy — it fundamentally rewired global supply chains. Every time a customer clicks "buy now" and expects next-day delivery, a warehouse somewhere has to fulfill that promise. According to industry research, every $1 billion in new e-commerce sales requires approximately 1.25 million square feet of warehouse and distribution space. With U.S. e-commerce sales surpassing $1 trillion annually, the math speaks for itself.

Major retailers and third-party logistics providers (3PLs) have aggressively expanded their footprints to keep up with consumer expectations. Companies like Amazon, Walmart, and Target have leased and developed millions of square feet of industrial space, pushing rents higher and absorption rates to record levels across nearly every major U.S. market.

Supply Chain Reshoring: A Structural Tailwind

Beyond e-commerce, a broader macroeconomic story is playing out. The COVID-19 pandemic exposed the fragility of global just-in-time supply chains, prompting U.S. companies to rethink their dependence on overseas manufacturing. The result? A massive wave of reshoring and nearshoring activity that is generating extraordinary demand for domestic industrial facilities.

- Manufacturing facilities are returning to American soil, particularly in semiconductor, pharmaceutical, and electric vehicle sectors.

- Nearshoring to Mexico is driving demand for industrial real estate along the U.S.-Mexico border corridor.

- "Safety stock" inventory strategies mean companies are now holding more goods domestically, requiring larger and more numerous warehousing facilities.

- Federal incentives through the CHIPS Act and Inflation Reduction Act are catalyzing billions in domestic manufacturing investment.

These aren't cyclical trends — they represent structural, long-term changes to how American businesses operate, and industrial real estate is the primary beneficiary.

Key Metrics That Make Warehouses So Attractive to Investors

Historic Low Vacancy Rates

National industrial vacancy rates have hovered near 3–5% in recent years — levels that give landlords tremendous pricing power. In key logistics hubs like the Inland Empire (California), Dallas-Fort Worth, Chicago, and New Jersey, vacancy has been even tighter, sometimes falling below 2%. For context, a "balanced" commercial real estate market typically sees vacancy around 8–10%.

Rent Growth Outpacing Other Asset Classes

Industrial asking rents have seen double-digit year-over-year growth in many markets, dramatically outpacing office, retail, and even multifamily in some regions. As leases signed during low-rent environments roll over to market rates, investors are capturing massive mark-to-market rent bumps — often 40–60% or more in high-demand submarkets.

Long-Term, Credit-Quality Tenants

Industrial properties often attract Fortune 500 companies, investment-grade logistics operators, and government-backed entities as tenants. These tenants sign longer leases (typically 5–15 years), provide stable, predictable cash flows, and maintain properties to operational standards. For investors seeking reliable income, this tenant profile is exceptionally compelling.

Relatively Low Capital Expenditure Requirements

Compared to office or retail properties, warehouses typically require less ongoing maintenance and tenant improvement investment. Their functional simplicity — clear-height ceilings, concrete floors, dock doors, and trailer parking — means fewer costly upgrades and lower operational overhead for property owners.

The Rise of Last-Mile Logistics Facilities

One of the fastest-growing sub-sectors within industrial real estate is last-mile logistics — smaller urban warehouses positioned within dense metropolitan areas to enable same-day and next-day delivery. As consumers increasingly demand near-instant fulfillment, retailers and logistics companies are racing to secure infill industrial sites closer to population centers.

These properties are often scarce, hard to replace (due to land constraints in urban areas), and command premium rents. Urban infill industrial assets in markets like Los Angeles, New York, Miami, and Seattle have seen some of the most aggressive rent appreciation in the entire real estate sector. For investors, this sub-sector represents a particularly attractive combination of scarcity value and strong demand fundamentals.

Cold Storage: The Specialized Industrial Opportunity

The pandemic also accelerated consumer adoption of grocery delivery and meal kit services, creating explosive demand for temperature-controlled warehousing — commonly known as cold storage. Cold storage facilities command significant rent premiums over traditional dry warehouses, and the supply of purpose-built facilities remains severely constrained.

Developers and investors who can navigate the higher construction costs and specialized operational requirements of cold storage are being rewarded with strong yields and a growing tenant base that spans food and beverage, pharmaceuticals, and biotechnology. If you're exploring industrial property listings with diversified income potential, cold storage is a category worth prioritizing in your research.

Top Industrial Real Estate Markets in the United States

Not all industrial markets are created equal. Several U.S. metros consistently rank as the most in-demand locations for warehouse and distribution investment:

- Dallas-Fort Worth, TX: Central U.S. location, business-friendly environment, and massive population growth make DFW a top-tier industrial hub.

- Inland Empire, CA: Gateway to the largest U.S. ports (Los Angeles and Long Beach), with unmatched distribution reach to Western markets.

- Chicago, IL: The Midwest's logistics nerve center, with unparalleled rail, highway, and air freight connectivity.

- New Jersey / Pennsylvania I-78/I-287 Corridor: Proximity to the Port of New York/New Jersey and 50+ million consumers within a one-day drive.

- Phoenix, AZ: A rapidly growing Sunbelt market attracting semiconductor manufacturing, data centers, and e-commerce distribution.

- Atlanta, GA: Southeast logistics hub with Hartsfield-Jackson Atlanta International Airport, the world's busiest, as a major freight catalyst.

- Nashville, TN: Emerging as a breakout market with central U.S. positioning and a booming consumer base.

How to Evaluate a Warehouse Investment

Location and Infill vs. Suburban Trade-offs

Proximity to transportation infrastructure — major highways, rail lines, ports, and airports — is the single most important factor in industrial real estate valuation. Infill locations near population centers command premium rents but come with higher acquisition costs and limited development opportunities. Suburban or exurban locations offer more affordable entry points and potential for land appreciation as metro areas expand.

Clear Height and Modern Specifications

Modern logistics operations increasingly require high-clear facilities — warehouses with 36-foot or greater ceiling heights — to accommodate high-bay racking systems and automation. Older facilities with 24-foot or lower clear heights may face functional obsolescence over time. When evaluating assets, always assess whether the building's specifications align with current and future tenant requirements.

Power Infrastructure

With the rise of automated distribution centers and electric vehicle charging facilities, robust electrical infrastructure has become a critical differentiator. Properties with significant power capacity (measured in megawatts) command higher rents and attract a wider pool of prospective tenants — from robotics-driven fulfillment operations to data center-adjacent facilities.

Lease Structure and Rollover Risk

Analyze the weighted average lease term (WALT), upcoming lease expirations, and rent escalation provisions carefully. Properties with near-term lease rollovers in high-rent-growth markets can represent significant upside — but also carry risk if market conditions soften. Triple-net (NNN) leases, where tenants cover taxes, insurance, and maintenance, are the gold standard for passive industrial investors.

Industrial REITs vs. Direct Ownership: Which Path Is Right for You?

Investors seeking exposure to industrial real estate have two primary vehicles: direct property ownership and industrial Real Estate Investment Trusts (REITs). Each approach offers distinct advantages and trade-offs:

- Direct Ownership: Maximum control, potential for value-add improvements, full capture of rent growth and appreciation, but requires significant capital, management resources, and market expertise.

- Industrial REITs: Prologis (PLD), Duke Realty (acquired by Prologis), EastGroup Properties (EGP), and STAG Industrial (STAG) offer liquid, diversified exposure to the sector with professional management — but at the cost of control and with some correlation to broader equity markets.

- Private Equity and Syndications: Pooled investment vehicles offer accredited investors access to institutional-quality deals with professional management and potentially higher returns than REITs, though with reduced liquidity.

For most individual investors, a combination of strategies — perhaps direct ownership of one or two well-located properties alongside REIT exposure — provides both active upside and diversified, passive income. Our team at Cordura can help you connect with the right properties and investment structures to match your goals and risk profile.

Challenges and Risks to Watch in the Industrial Sector

No asset class is without risk, and industrial real estate is no exception. Investors should be aware of several evolving headwinds:

- Supply deliveries: The development pipeline expanded significantly in 2022–2023, with millions of new square feet delivering in some markets. This has begun to moderate rent growth in certain submarkets, though absorption has remained healthy overall.

- Interest rate sensitivity: Rising borrowing costs compress returns and have pushed cap rates modestly higher from their record lows. Investors must underwrite conservatively and stress-test financing assumptions.

- Market-specific oversupply: Some secondary markets saw speculative overdevelopment; careful submarket selection remains critical.

- Environmental and zoning regulations: Industrial development faces increasing community opposition in some regions, particularly around truck traffic and air quality concerns, which can constrain supply and affect permitting timelines.

Despite these considerations, the long-term demand drivers for industrial real estate remain firmly intact. Experienced investors view current market normalization not as a retreat, but as a healthier, more sustainable growth trajectory following several years of extraordinary performance.

The Future of Industrial Real Estate: Automation, Robotics, and PropTech

Looking ahead, industrial real estate will increasingly intersect with advanced technology. Automated storage and retrieval systems (AS/RS), robotic picking and packing, and AI-driven inventory management are transforming the physical requirements of warehouse space. This is creating a bifurcation in the market: state-of-the-art, technology-ready facilities are attracting premium tenants and commanding top rents, while older, functionally obsolete buildings face growing pressure to adapt or be repurposed.

Investors who prioritize modern specifications, adequate power capacity, and flexibility of use will be best positioned to capitalize on the next wave of industrial demand. The warehouses being built and upgraded today are not passive storage boxes — they are sophisticated, technology-enabled fulfillment engines at the heart of the modern economy.

Why Cordura Is Your Partner in Industrial Real Estate

At Cordura, we specialize in helping investors, buyers, and property seekers navigate the dynamic U.S. commercial real estate market with confidence. Our deep market expertise, data-driven approach, and nationwide network of industrial properties give our clients a decisive edge in identifying, evaluating, and acquiring warehouse assets that deliver strong, risk-adjusted returns.

Whether you're looking for a stabilized NNN warehouse in a top logistics corridor, a value-add distribution center with near-term rent upside, or a ground-up development opportunity in an emerging industrial market, Cordura has the resources and relationships to help you succeed. Industrial real estate's moment is now — and with the right guidance, your portfolio can be a direct beneficiary of one of the most powerful demand stories in modern commercial real estate history.