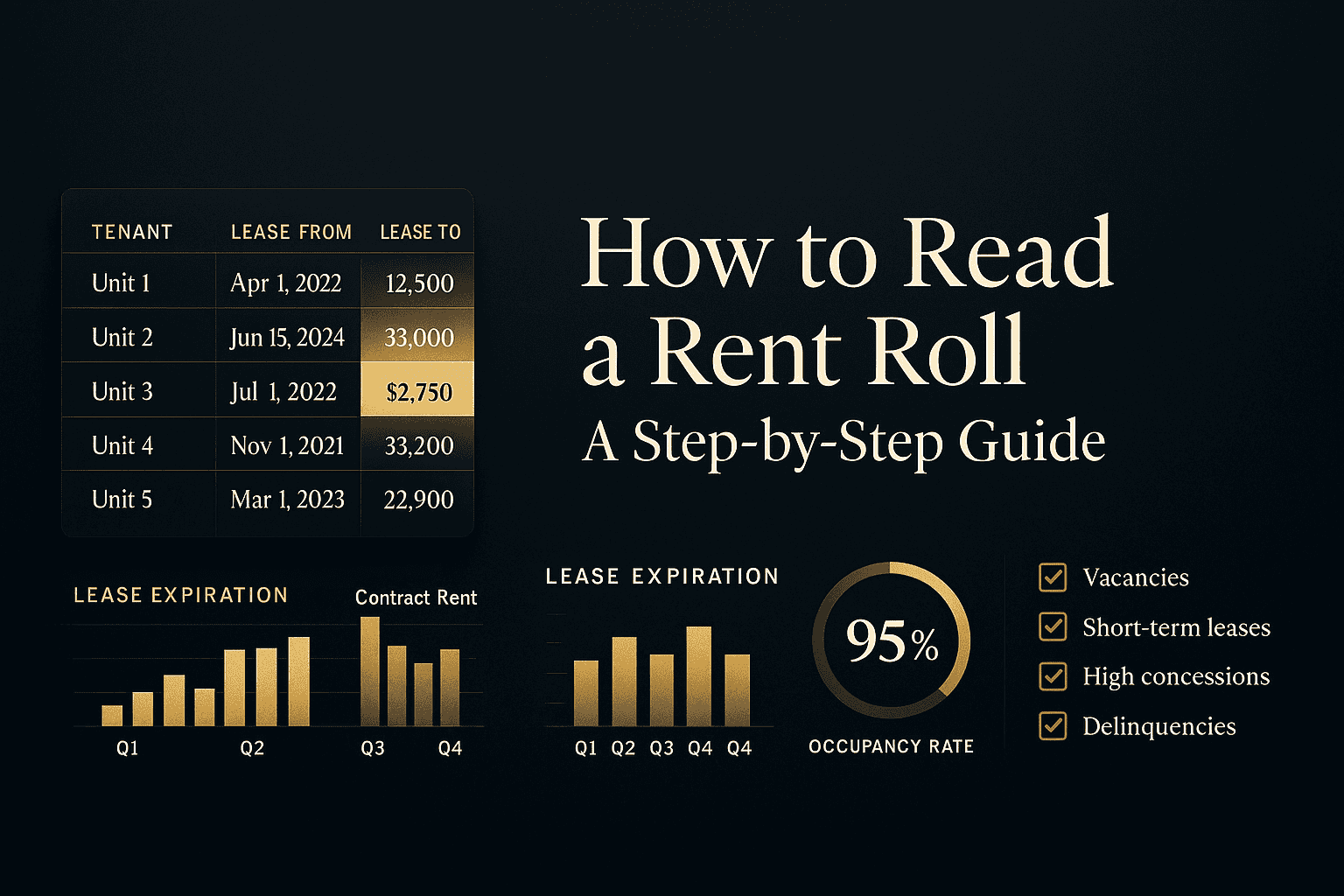

How to Read a Rent Roll: A Step-by-Step Guide for Commercial Real Estate Investors

Whether you're evaluating your first multifamily property or expanding a commercial portfolio, understanding how to read a rent roll is one of the most essential skills in real estate investing. A rent roll is far more than a simple list of tenants — it's a financial snapshot of a property's income-producing potential, occupancy health, and lease risk profile.

At Cordura, we work with investors and buyers across the US market who rely on accurate rent roll analysis to make confident, data-driven acquisition decisions. This step-by-step guide will walk you through exactly what a rent roll contains, how to interpret each section, and what red flags to watch for before closing a deal.

What Is a Rent Roll?

A rent roll is a document — typically provided by a property owner or management company — that summarizes all current leases and rental income for a property. It consolidates tenant information, lease terms, monthly rent, and occupancy status into a single, structured format.

Lenders, buyers, and investors use the rent roll during due diligence to verify a property's current and projected income. Without a thorough rent roll review, you may be relying on pro forma projections that don't reflect reality.

Step 1: Understand the Standard Components of a Rent Roll

Before diving into analysis, familiarize yourself with what a complete rent roll should include. While formats can vary, most rent rolls for commercial and multifamily properties contain the following columns:

- Unit or Suite Number: Identifies each rentable space on the property.

- Tenant Name: The legal name of the occupying tenant or business.

- Lease Start Date: When the current lease term began.

- Lease Expiration Date: When the current lease is scheduled to end.

- Monthly Rent (Contract Rent): The amount the tenant is contractually obligated to pay each month.

- Market Rent: The estimated rent the unit could achieve at current market rates.

- Square Footage: The rentable square footage of each unit or suite.

- Rent per Square Foot: Monthly or annual rent divided by square footage, useful for comparisons.

- Security Deposit: Amount held on deposit from each tenant.

- Occupancy Status: Whether the unit is occupied, vacant, or under notice.

- Late Fees or Delinquencies: Any outstanding balances owed by tenants.

- Lease Type: Gross, net, NNN, modified gross, or other lease structures.

If a rent roll is missing any of these components, request a more complete version before proceeding with your analysis.

Step 2: Calculate Gross Potential Rent (GPR)

Once you have the full rent roll in hand, your first calculation should be Gross Potential Rent (GPR) — the total income the property would generate if every unit were leased at its contract rent with zero vacancies.

To calculate GPR, simply add up all monthly contract rents across every unit and multiply by 12 for an annual figure:

- Sum of all monthly contract rents = Monthly GPR

- Monthly GPR × 12 = Annual GPR

GPR represents the ceiling of income potential. From here, you'll make deductions for vacancies, concessions, and credit losses to arrive at Effective Gross Income (EGI).

Step 3: Assess Occupancy Rate and Vacancy

The occupancy rate is one of the first metrics buyers look at when reviewing a rent roll. A high occupancy rate signals a healthy, in-demand property, while persistent vacancies may indicate pricing issues, deferred maintenance, or location challenges.

To calculate occupancy rate from the rent roll:

- Occupancy Rate = (Number of Occupied Units / Total Units) × 100

For example, if a 20-unit apartment building has 18 occupied units, the occupancy rate is 90%. While 90–95% is generally considered healthy for multifamily assets, the benchmark varies by property type and market.

Don't just look at current occupancy — ask for historical rent rolls to understand whether vacancies are a short-term anomaly or a persistent trend. If the seller can only provide one snapshot in time, that's a red flag worth noting during commercial real estate due diligence.

Step 4: Review Lease Expiration Dates and Rollover Risk

One of the most overlooked aspects of rent roll analysis is lease rollover risk — the risk that multiple leases expire around the same time, exposing you to potential vacancy or the need for significant re-leasing costs.

When reviewing lease expiration dates, create a rollover schedule:

- List the expiration month and year for every lease.

- Group them by quarter or year to identify concentration risk.

- Flag any leases expiring within 12 months of your projected acquisition date.

If 40% of your leases expire in the same year, you're taking on significant income volatility. Ideally, you want a staggered lease expiration profile that smooths out renewal risk over time.

Also pay close attention to month-to-month tenants. These arrangements provide flexibility for the tenant — but not for you as the new owner. A high percentage of month-to-month leases can signal tenant instability or a seller who avoided locking in long-term agreements to inflate short-term occupancy numbers.

Step 5: Compare Contract Rent to Market Rent

The gap between contract rent (what tenants currently pay) and market rent (what the market would support) reveals your potential upside or downside risk.

- Below-Market Rents: If contract rents are significantly below market, you may have rent growth upside as leases roll over. However, below-market rents can also indicate long-term tenants who may resist increases or have legal protections in rent-stabilized markets.

- Above-Market Rents: Rents above current market rates are a red flag. When these leases expire, tenants may leave or demand lower rents, putting downside pressure on your income projections.

- At-Market Rents: Leases priced at current market rates offer the most predictable cash flow with limited upside — but also limited risk.

Always verify market rent assumptions independently using local comparable data, not just the seller's pro forma. This comparison is a critical component of any investment property analysis.

Step 6: Evaluate Tenant Credit Quality and Mix

For commercial properties — including retail, office, and industrial — the creditworthiness of your tenants directly impacts the stability of your income stream. A single-tenant building anchored by a Fortune 500 company carries far less income risk than a multi-tenant strip center with local mom-and-pop operators.

When reviewing the rent roll for commercial assets, assess:

- Anchor tenants: Are there any national or credit tenants occupying significant square footage?

- Tenant concentration risk: Does one tenant represent more than 20–30% of total rental income? If so, their departure creates an outsized income disruption.

- Business type and sector: Are tenants in stable industries or volatile ones? Retail and food service carry higher turnover risk than medical or professional services.

- Lease guarantees: Are leases personally guaranteed or backed by a parent company?

Step 7: Check for Delinquencies and Outstanding Balances

A rent roll should reflect not just what tenants owe, but what they actually pay. Review any delinquency column carefully — tenants with outstanding balances can reduce the actual cash flow you'll receive on Day 1 of ownership.

Ask the seller or property manager for an accounts receivable aging report alongside the rent roll. This report shows how long outstanding balances have been unpaid, categorized by 30, 60, 90, and 90+ days past due. Chronic late payers or tenants with 60+ day delinquencies represent collection risk that should factor into your pricing and due diligence.

During lease review, also check whether the existing leases include strong late fee provisions and whether those fees have actually been enforced. Lax enforcement often signals management deficiencies that a new owner will need to address.

Step 8: Analyze Lease Types and Expense Responsibilities

The lease structure determines who pays for what — and it has a significant impact on your net operating income. The most common commercial lease types include:

- Gross Lease: The landlord pays most operating expenses (taxes, insurance, maintenance). Higher rent, but more landlord exposure to rising costs.

- Net Lease (Single, Double, Triple): Tenants pay some or all operating expenses in addition to base rent. NNN leases offer the most landlord protection from expense increases.

- Modified Gross Lease: A hybrid where some expenses are split between landlord and tenant by negotiation.

A rent roll alone won't always show the lease type — you'll need to cross-reference the actual lease documents. But the rent roll should indicate whether any gross or net arrangements are in place, and this will affect how you model your NOI and cash-on-cash return.

Step 9: Verify Rent Roll Accuracy Through Third-Party Sources

Never take a rent roll at face value. Sellers have a financial incentive to present their property in the best possible light, and inaccuracies — whether intentional or unintentional — can be costly after closing.

To verify rent roll accuracy:

- Request estoppel certificates from each tenant, confirming their lease terms, rent amount, and any landlord obligations or disputes.

- Review bank statements showing 12–24 months of rent deposits to confirm actual collections match rent roll figures.

- Compare against tax returns — the Schedule E (for residential) or business tax returns should reflect rental income consistent with the rent roll.

- Conduct tenant interviews (with seller permission) to confirm terms directly.

- Hire a third-party property manager to review the roll and flag anomalies based on local market knowledge.

Step 10: Build Your Pro Forma From the Rent Roll

With a verified, fully analyzed rent roll, you're now ready to build a credible pro forma income statement. The rent roll feeds directly into your income projections:

- Gross Potential Rent (GPR) — from contract rents

- Less: Vacancy and Credit Loss — typically 5–10% depending on market and asset class

- Less: Concessions — any free rent or move-in specials currently in place

- = Effective Gross Income (EGI)

- Less: Operating Expenses — adjusted based on lease types and actual cost data

- = Net Operating Income (NOI)

Your NOI, divided by your target cap rate, gives you a supportable valuation for the property. The rent roll is the foundation of this entire calculation — which is why accuracy in Step 9 is non-negotiable.

Common Rent Roll Red Flags to Watch For

As you work through the rent roll, keep an eye out for these warning signs that deserve further investigation:

- Unusually high occupancy right before a sale (potential stuffing with short-term tenants)

- Many leases expiring within 6–12 months of the listing date

- Large rent increases in the 12 months preceding the sale without corresponding market evidence

- Tenants paying significantly above market with no clear justification

- Missing or incomplete lease documentation for any unit

- High concentration of month-to-month tenancies

- Inconsistencies between the rent roll and the property's actual bank deposits

- Related-party tenants (family members or business associates of the seller renting at favorable rates)

If you encounter multiple red flags, consider adjusting your offer price, requesting seller escrow for contingencies, or walking away from the deal entirely. A thorough rent roll review can save you from acquiring a property with hidden income instability.

Rent Roll Analysis for Different Property Types

Multifamily Properties

For apartment buildings and multifamily assets, the rent roll focuses heavily on unit mix, individual unit rents vs. market, lease terms, and vacancy rates. Given the volume of tenants, pattern recognition is key — look for systemic issues rather than isolated ones.

Retail Properties

Retail rent rolls require close attention to percentage rent clauses (where tenants pay a base rent plus a percentage of gross sales), co-tenancy clauses (which allow tenants to reduce rent if an anchor leaves), and lease options that could affect your exit strategy. Explore our resources on commercial real estate listings to see how retail assets are marketed to buyers.

Office Properties

Office rent rolls demand scrutiny of lease lengths, expense stop provisions, and the creditworthiness of individual tenants. The post-pandemic office market has introduced higher sublease risk and shorter lease terms, making rollover analysis even more important.

Industrial Properties

Industrial assets often feature NNN leases with long durations and creditworthy tenants. The rent roll analysis here focuses on lease length, rental escalation clauses, and clear height or dock door specifications that affect re-leasing feasibility.

Final Thoughts: The Rent Roll Is Your Due Diligence Foundation

Learning how to read a rent roll is not just a technical skill — it's an investor mindset. Every number on that document represents real income, real risk, and real decision-making power. By taking a systematic, skeptical approach to rent roll analysis, you protect yourself from overpaying for a property and position yourself to underwrite deals with confidence.

At Cordura, we believe that informed investors make better decisions. Whether you're analyzing a 10-unit apartment complex or a 100,000-square-foot commercial center, the principles in this guide apply. Take your time, verify your data, and never let an attractive pro forma substitute for a thorough rent roll review.

Ready to put these skills to work? Browse our current commercial property listings and start applying your rent roll analysis framework today.