How Interest Rates Shape the Commercial Real Estate Landscape

Few economic forces influence commercial real estate as profoundly as interest rates. Whether you're an investor evaluating a new acquisition, a developer planning a project, or a business owner searching for the right property, understanding how interest rate movements ripple through the commercial real estate market is essential to making informed decisions. At Cordura, we help our clients navigate these complexities with clarity and confidence.

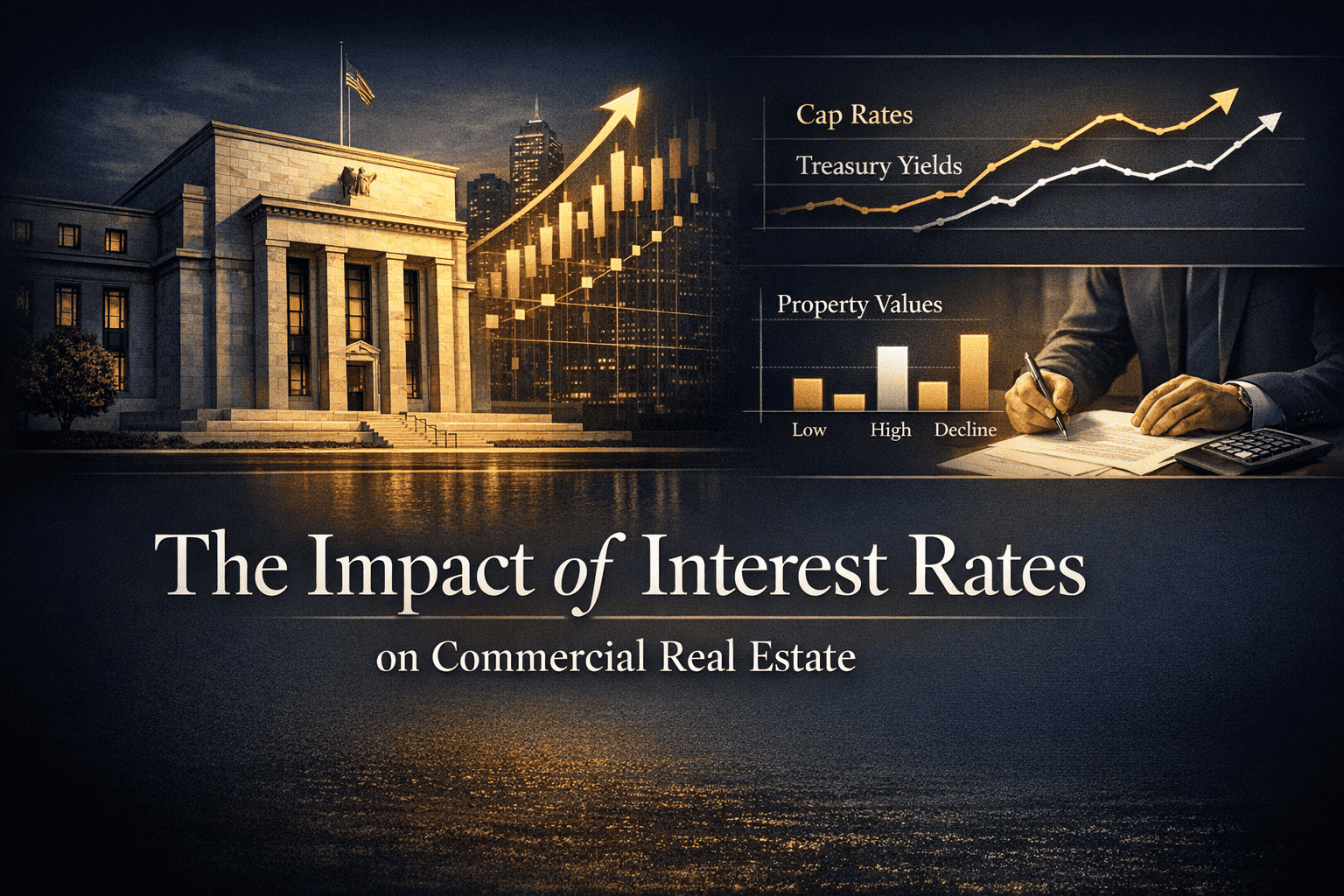

When the Federal Reserve adjusts benchmark interest rates, the effects are felt almost immediately across every asset class — and commercial real estate is no exception. From cap rate compression to financing costs and property valuations, interest rates are one of the most powerful variables in the CRE equation.

The Relationship Between Interest Rates and Cap Rates

One of the most direct connections in commercial real estate is between interest rates and capitalization rates (cap rates). Cap rates represent the expected return on a property based on its net operating income relative to its value. Historically, cap rates and interest rates move in the same direction — when rates rise, cap rates tend to follow, which puts downward pressure on property values.

Here's why: as borrowing costs increase, investors require higher yields to justify their risk exposure. If a 10-year Treasury bond yields 5%, why would an investor accept a 4.5% cap rate on an office building? This dynamic forces property prices to adjust downward until cap rates reflect a sufficient risk premium over the risk-free rate.

- Rising rates generally compress property valuations as buyers demand higher yields

- Falling rates support higher valuations by making debt cheaper and yields relatively more attractive

- Stable rates create predictable market conditions, encouraging transaction volume

Understanding this relationship is critical for investors evaluating commercial real estate investment opportunities in any rate environment.

Impact on Financing and Debt Costs

Interest rates directly determine the cost of debt, which is the lifeblood of most commercial real estate transactions. When rates are low, investors can leverage their capital more aggressively, financing a greater portion of a purchase at manageable debt service costs. When rates climb, the same property may produce insufficient cash flow to support the same loan amount.

Fixed vs. Variable Rate Loans

The structure of a loan matters enormously in a shifting rate environment. Fixed-rate loans provide certainty but may come at a premium. Variable-rate loans — often tied to SOFR or the prime rate — can offer lower initial costs but expose borrowers to payment increases if rates rise unexpectedly. Many commercial real estate investors who secured variable-rate debt during the low-rate era of 2020–2021 faced significant refinancing challenges as rates surged through 2022 and 2023.

Debt Service Coverage Ratio (DSCR) Under Pressure

Lenders evaluate loans based on DSCR — the ratio of net operating income to annual debt service. As interest rates increase, debt service payments grow, compressing DSCR and making it harder to qualify for financing. This effectively reduces purchasing power across the board and can stall deal activity, particularly for assets with thin margins.

Sector-by-Sector Effects of Rate Changes

Not all commercial real estate sectors respond to interest rate changes in the same way. The sensitivity varies depending on lease structures, income stability, and underlying demand drivers.

Office and Retail Properties

Office and retail assets tend to be more sensitive to interest rate hikes because they often carry longer vacancy risks and higher capital expenditure requirements. Rising rates increase the cost of repositioning these assets, making value-add plays more challenging to underwrite.

Industrial and Logistics Properties

Industrial real estate has demonstrated relative resilience in rising rate environments, largely due to robust demand from e-commerce and supply chain restructuring. Strong rent growth in this sector has helped offset yield compression pressures, maintaining investor appetite even as borrowing costs increase.

Multifamily and Mixed-Use

Multifamily properties benefit from shorter lease durations, allowing owners to reset rents more frequently in response to inflation — which often accompanies rising rates. However, high rates can dampen transaction volume as buyers and sellers struggle to agree on pricing. Explore our multifamily and mixed-use properties listings to discover opportunities across key US markets.

Hospitality and Special Purpose

Hospitality assets, driven by RevPAR and occupancy trends, can be insulated from rate impacts if travel demand remains strong. However, the capital-intensive nature of these properties makes financing more critical, and rising rates can significantly impact hotel transaction activity.

Interest Rates and Commercial Real Estate Valuations

Property valuations in commercial real estate are ultimately driven by income potential discounted at an appropriate rate. When interest rates rise, discount rates rise with them, reducing the present value of future cash flows. This mathematical reality means that even a stable, well-leased property can see its appraised value decline in a high-rate environment — not because anything changed operationally, but because the cost of capital increased.

Investors using discounted cash flow (DCF) analysis will recognize this effect immediately: a 100-basis-point increase in the discount rate applied to a 10-year hold can reduce a property's estimated value by 8–15%, depending on the income profile. This is why many commercial real estate deals that penciled out in 2021 simply don't work at 2023–2024 rate levels without price adjustments from sellers.

Strategies for Navigating a High-Rate Environment

While rising interest rates present challenges, savvy commercial real estate professionals adapt their strategies to find value in any market cycle. Here are proven approaches to consider:

- Focus on cash-flowing assets: Prioritize properties with strong in-place income and creditworthy tenants that can sustain debt service even at higher rates

- Negotiate seller financing: In high-rate environments, some sellers may offer favorable financing to facilitate transactions, effectively bridging the gap between market rates and deal economics

- Shorten hold periods or increase yield targets: Adjust your return expectations to account for higher capital costs by targeting assets with upside in rents or occupancy

- Explore bridge-to-agency strategies: For multifamily, using short-term bridge loans with a plan to refinance into agency debt when rates normalize can preserve flexibility

- Look at distressed opportunities: Rate-driven market stress creates acquisition opportunities for well-capitalized buyers with access to capital

Our advisors at Cordura work closely with clients to tailor acquisition and portfolio strategies to current market conditions. Learn more about commercial real estate market trends to stay ahead of the curve.

The Fed's Role and What Investors Should Watch

The Federal Open Market Committee (FOMC) sets the federal funds rate, which influences short-term borrowing costs across the economy. While the Fed doesn't directly set mortgage rates, its decisions cascade through SOFR, the prime rate, Treasury yields, and ultimately into CRE lending rates. Investors who monitor FOMC meeting outcomes, inflation data (CPI and PCE), and employment reports gain a meaningful edge in anticipating market shifts.

Key indicators to track include:

- Federal funds rate decisions and forward guidance from the Fed

- 10-year and 5-year Treasury yield movements

- SOFR rates for variable-rate loan benchmarking

- Inflation metrics (CPI, PCE) that drive Fed policy decisions

- Commercial mortgage-backed securities (CMBS) spreads as a sign of lender risk appetite

Looking Ahead: Opportunities in a Normalizing Rate Environment

As the Federal Reserve signals potential rate cuts in response to cooling inflation, commercial real estate markets are beginning to anticipate a new cycle. Historical data shows that the 12–18 months following peak rate environments have often been among the most productive periods for commercial real estate acquisitions, as sellers become more flexible and buyer competition remains muted.

For investors with dry powder and the analytical framework to evaluate deals accurately, today's market presents a compelling entry point. Properties that struggled to transact during peak uncertainty may soon see renewed interest as financing costs ease and bid-ask spreads narrow.

At Cordura, we believe informed investors who understand macroeconomic drivers — including the impact of interest rates — are best positioned to build lasting wealth through commercial real estate. Whether you're entering the market for the first time or expanding an existing portfolio, our team is here to guide you every step of the way.