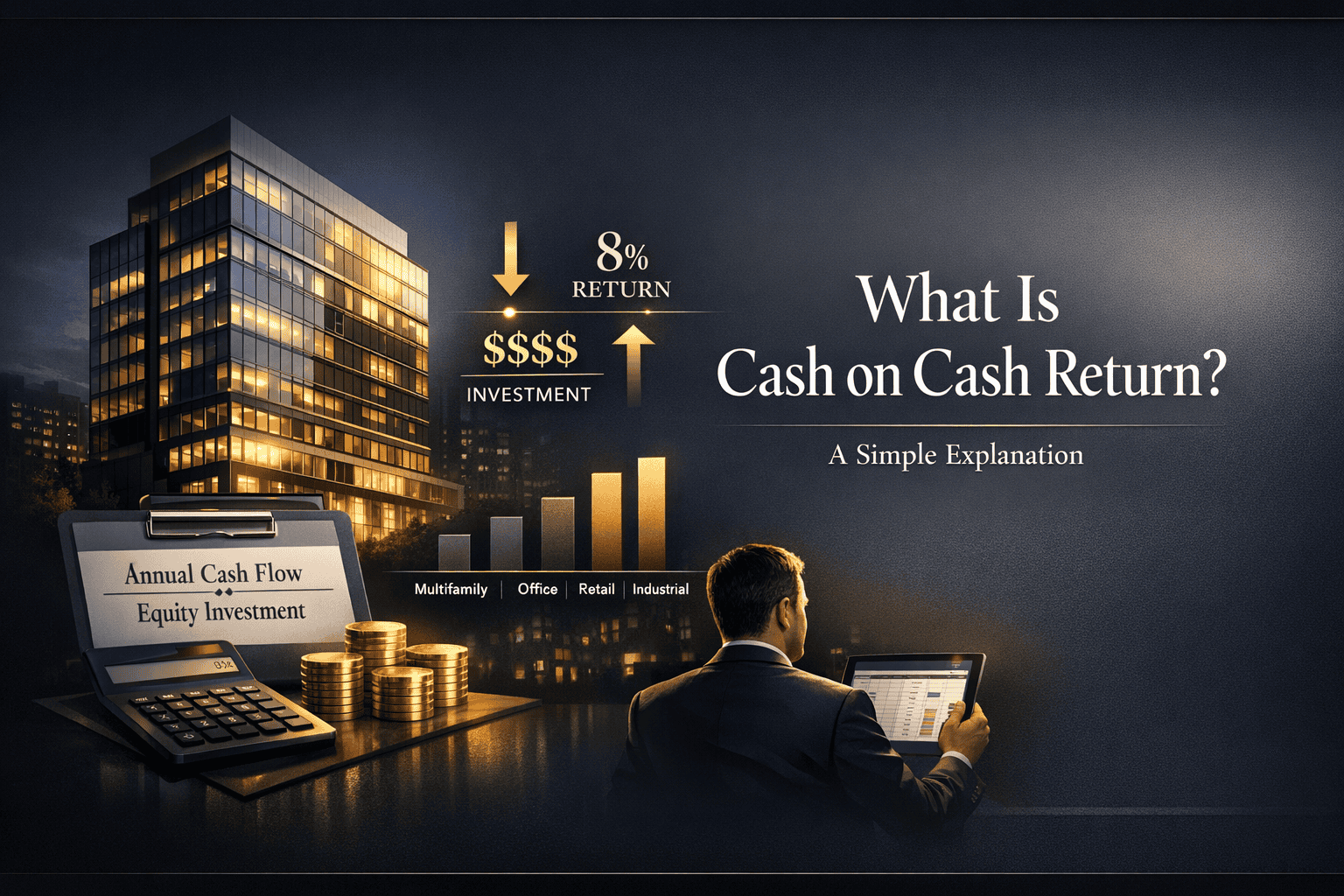

What Is Cash on Cash Return? A Simple Explanation for Real Estate Investors

If you're exploring commercial real estate investments, you've likely come across the term cash on cash return. It's one of the most widely used metrics in the industry — and for good reason. Understanding this figure can mean the difference between a smart investment and a costly mistake. At Cordura, we believe every investor deserves clear, actionable knowledge before committing capital. This guide breaks down exactly what cash on cash return means, how to calculate it, and why it matters for your portfolio.

Cash on Cash Return: The Core Definition

Cash on cash return (CoC return) is a financial metric used to measure the annual pre-tax cash income earned on the actual cash invested in a property. Unlike other return metrics that account for appreciation or tax benefits, cash on cash return focuses purely on cash flow relative to cash invested. This makes it especially useful for comparing investment opportunities on a straightforward, apples-to-apples basis.

In simple terms: it tells you how many dollars you're getting back each year for every dollar you put in — based solely on real cash in your pocket.

The Cash on Cash Return Formula

The formula is refreshingly simple:

- Cash on Cash Return = Annual Pre-Tax Cash Flow ÷ Total Cash Invested × 100

Let's define each component:

- Annual Pre-Tax Cash Flow: The total rental income received in a year, minus all operating expenses (mortgage payments, property management fees, maintenance, insurance, taxes, and vacancies).

- Total Cash Invested: The actual out-of-pocket cash you invested, including your down payment, closing costs, and any upfront renovation or improvement costs.

Cash on Cash Return Example

Let's walk through a real-world scenario to make this concrete.

Imagine you purchase a small commercial office building for $800,000. You put down $200,000 (25%) and finance the rest. After accounting for all closing costs and initial improvements, your total cash invested is $220,000.

The property generates $90,000 per year in gross rental income. After deducting operating expenses (mortgage payments, property taxes, insurance, maintenance, and management fees) totaling $68,000, your annual pre-tax cash flow is $22,000.

Plugging into the formula:

- $22,000 ÷ $220,000 × 100 = 10% Cash on Cash Return

A 10% CoC return means you're earning 10 cents in cash for every dollar you invested each year — a solid benchmark in many commercial markets.

What Is a Good Cash on Cash Return?

There's no single universal answer, as "good" depends on the market, property type, and your investment goals. However, here are some general benchmarks investors use:

- 5–7%: Acceptable in high-demand, low-risk markets (e.g., major metros with stable tenants)

- 8–12%: Strong return, often targeted by active commercial investors

- 12%+: Excellent, but typically comes with higher risk or value-add potential

It's also important to compare your CoC return against alternative investments. If a risk-free Treasury bond yields 5%, a commercial property offering 6% CoC might not justify the added complexity and risk. Context always matters.

If you're evaluating properties across different markets, our commercial real estate listings provide detailed financial breakdowns to help you compare opportunities side by side.

Cash on Cash Return vs. Other Metrics

Cash on Cash Return vs. Cap Rate

The capitalization rate (cap rate) measures a property's net operating income (NOI) relative to its purchase price — without factoring in financing. Cash on cash return, by contrast, accounts for your actual financing terms and the specific cash you put in. Two investors buying the same property with different down payments will have different CoC returns but the same cap rate.

Cash on Cash Return vs. ROI

Return on Investment (ROI) is broader — it typically includes appreciation, equity buildup, and tax benefits alongside cash flow. Cash on cash return is narrower and more immediate: it only measures what's hitting your bank account each year relative to your cash investment. For investors focused on short-to-medium-term cash flow, CoC return is often the more practical metric.

Cash on Cash Return vs. Internal Rate of Return (IRR)

IRR accounts for the time value of money and factors in your full investment lifecycle, including the eventual sale proceeds. Cash on cash return is a simpler, annual snapshot. Many sophisticated investors use both: CoC for year-by-year cash flow analysis and IRR for evaluating the full investment horizon.

Why Cash on Cash Return Matters in Commercial Real Estate

Commercial real estate investing is fundamentally a cash flow business. Unlike residential properties, commercial assets are valued largely on the income they generate. Here's why CoC return is especially critical in this space:

- Financing impact is significant: Commercial loans often have different structures than residential mortgages. A higher interest rate or shorter amortization period can dramatically affect your CoC return, even if the property itself performs well.

- Leverage analysis: CoC return helps you understand whether using debt is actually improving your returns. When your CoC return exceeds your mortgage interest rate, leverage is working in your favor — known as positive leverage.

- Investor communication: For syndications or partnerships, CoC return is often the first metric limited partners ask about. It's a clear, tangible promise: "Here's the annual cash yield on your investment."

- Decision speed: When evaluating multiple properties quickly, CoC return allows for fast, efficient comparisons without complex modeling.

To understand how financing structures affect your returns, explore our commercial real estate financing resources for guidance tailored to US investors.

Limitations of Cash on Cash Return

While cash on cash return is a powerful tool, it's not without limitations. Every savvy investor should understand what it doesn't capture:

- Ignores appreciation: A property in a high-growth market may deliver modest CoC returns today but generate substantial equity gains over time. CoC alone would undervalue such an opportunity.

- Excludes tax benefits: Depreciation deductions and other tax advantages can significantly enhance your effective return — none of which appear in the CoC figure.

- Point-in-time snapshot: CoC return reflects one year's performance. It doesn't account for rent escalations, lease renewals, or market shifts that could improve or erode returns over time.

- Assumes stable cash flow: Vacancies, unexpected repairs, or tenant defaults can disrupt cash flow. CoC return based on projections may not reflect real-world performance.

For these reasons, professional investors typically use CoC return as one component of a broader due diligence framework — not as a standalone decision-maker.

How to Improve Your Cash on Cash Return

If you're analyzing a property with a lower-than-desired CoC return, there are several strategies to potentially improve it:

- Increase rental income: Identify below-market rents and plan for lease renewals at higher rates. Value-add properties often present this opportunity.

- Reduce operating expenses: Audit current management costs, insurance premiums, and maintenance contracts. Small savings compound quickly.

- Optimize financing: Securing a lower interest rate or longer amortization period reduces your annual debt service, directly improving cash flow.

- Minimize vacancy: Long-term, creditworthy tenants improve both cash flow predictability and your CoC return. Tenant quality matters as much as rent levels.

- Negotiate purchase price: A lower acquisition price reduces your total cash invested — directly improving the denominator in the CoC formula.

Using Cash on Cash Return in Your Investment Strategy

Whether you're a first-time commercial buyer or an experienced investor expanding your portfolio, cash on cash return should be a core part of your analysis toolkit. Here's a practical approach:

- Set a minimum CoC return threshold before you start shopping — this filters out properties that don't meet your cash flow needs from day one.

- Run sensitivity analyses by adjusting vacancy rates, rent levels, and interest rates to understand how resilient the return is under different scenarios.

- Compare CoC returns across property types — multifamily, retail, industrial, and office assets often trade at different CoC benchmarks due to risk profiles and market dynamics.

- Revisit your CoC assumptions annually as rents, expenses, and market conditions evolve.

Ready to find commercial properties with strong cash-on-cash potential? Browse our curated investment properties across top US markets, complete with financial performance data to support your analysis.

Final Thoughts: Cash on Cash Return as Your Investment Compass

Cash on cash return is one of the most intuitive and practical metrics available to commercial real estate investors. It cuts through complexity and answers the fundamental question every investor has: How much cash am I actually making on my cash?

By mastering this metric — understanding how to calculate it, what benchmarks to target, and how it fits alongside other measures like cap rate and IRR — you'll be better equipped to evaluate opportunities with confidence and clarity.

At Cordura, we're committed to empowering investors with the knowledge and tools to make smarter real estate decisions. Whether you're evaluating your first commercial acquisition or optimizing an existing portfolio, our team is here to guide you every step of the way.