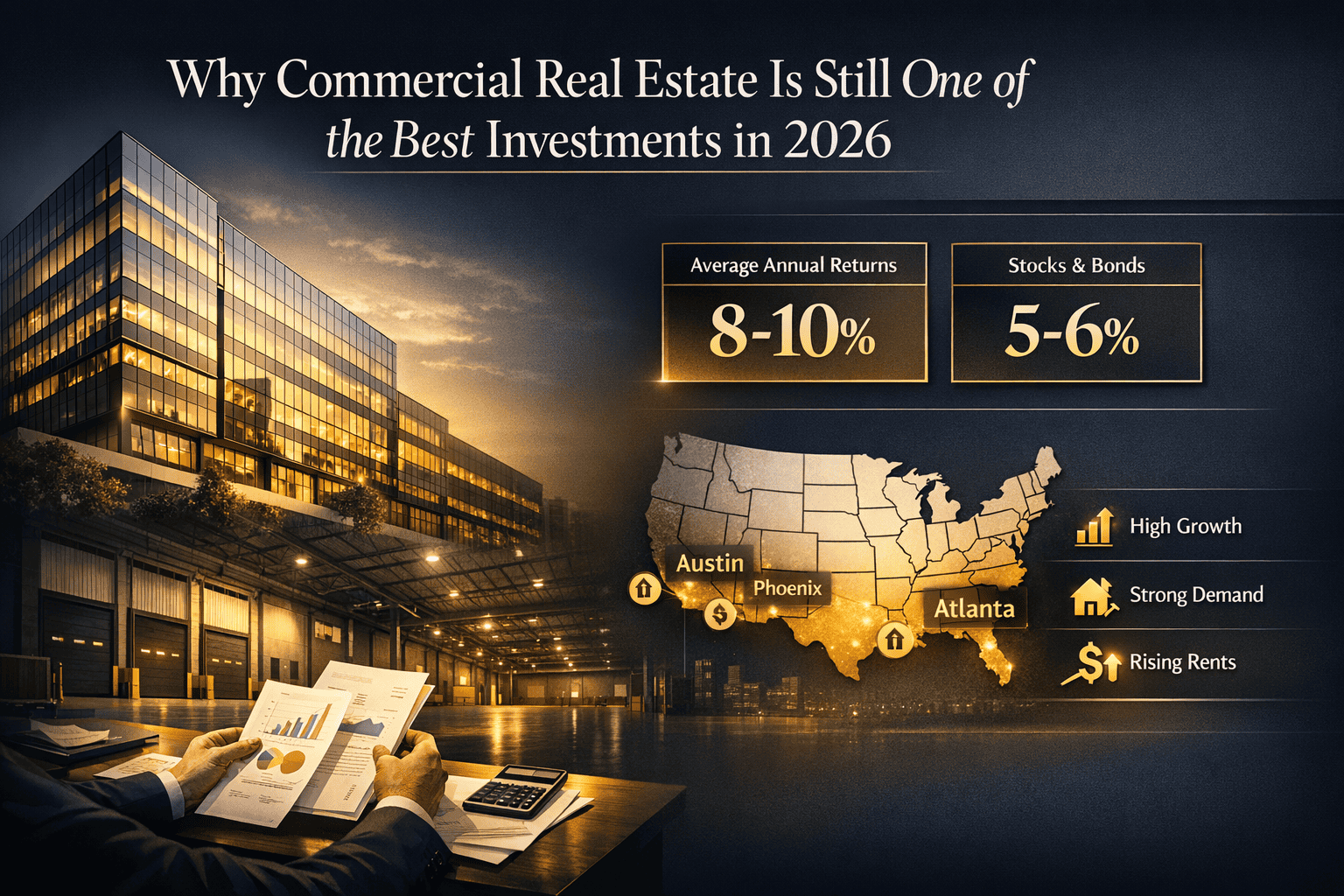

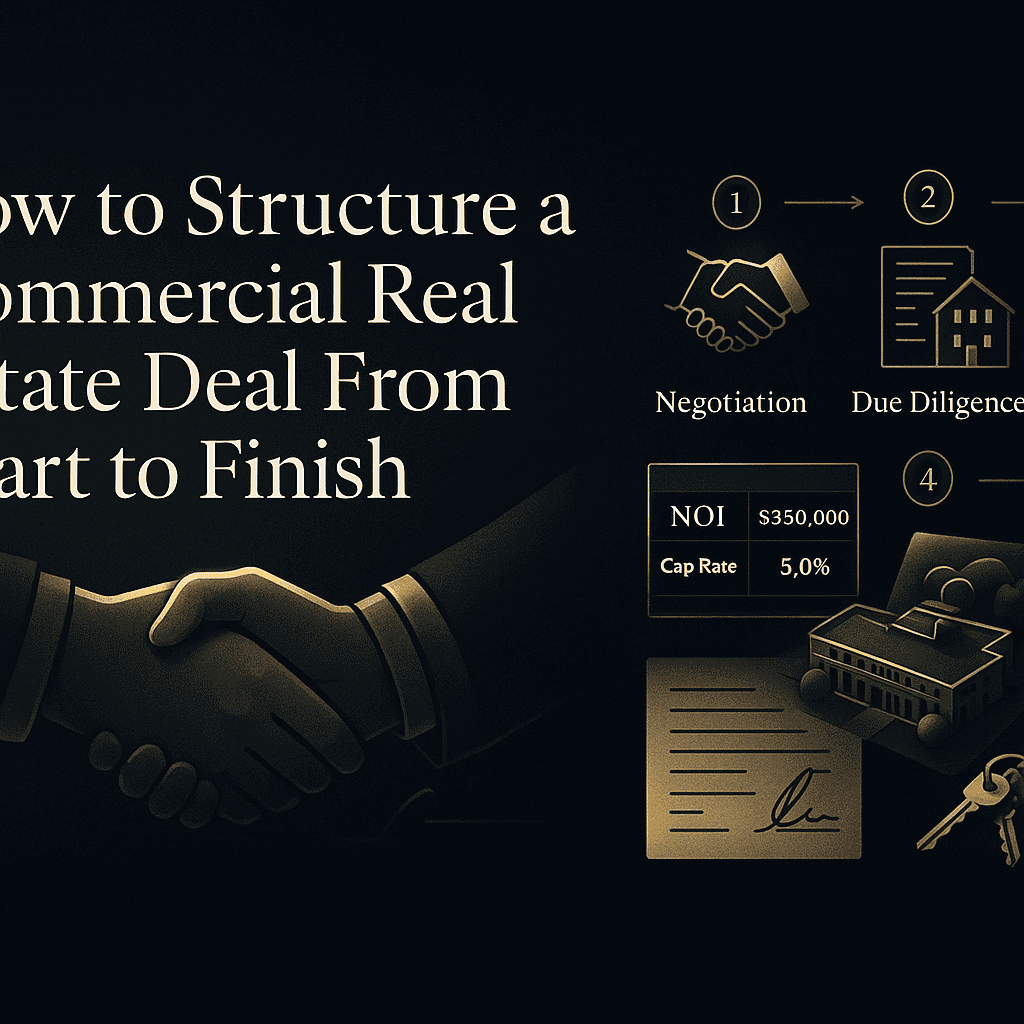

How to Structure a Commercial Real Estate Deal From Start to Finish

Structuring a commercial real estate deal is one of the most complex — and rewarding — processes in the world of investing. Whether you're acquiring an office building, a retail strip center, or a multifamily complex, having a clear, step-by-step framework can be the difference between a profitable transaction and a costly mistake. At Cordura, we work with investors, buyers, and property seekers across the US market to navigate every stage of the deal process with confidence.

In this guide, we'll walk you through the complete lifecycle of a commercial real estate deal — from identifying the right opportunity to closing the transaction and beyond.

Step 1: Define Your Investment Objectives

Before you even begin searching for a property, you need to establish clear investment goals. Ask yourself the following questions:

- Are you looking for long-term appreciation, stable cash flow, or both?

- What asset class interests you most — office, retail, industrial, multifamily, or mixed-use?

- What is your risk tolerance and investment horizon?

- How much capital do you have to deploy, and what is your target return?

Your answers will shape every decision you make throughout the deal process. Investors seeking passive income, for example, may prioritize net-leased properties with long-term tenants, while value-add investors might look for underperforming assets with repositioning potential.

Step 2: Assemble Your Deal Team

Commercial real estate is a team sport. The strength of your advisory team can significantly impact your ability to identify, negotiate, and close a deal successfully. A well-rounded team typically includes:

- Commercial Real Estate Broker: Provides market expertise, access to listings, and negotiation support.

- Real Estate Attorney: Handles contract review, due diligence, and closing documentation.

- Commercial Lender or Mortgage Broker: Structures financing and secures loan commitments.

- CPA or Tax Advisor: Identifies tax implications, including depreciation and 1031 exchange opportunities.

- Property Inspector and Environmental Consultant: Assesses physical condition and environmental risks.

Building relationships with experienced professionals early in the process will save you time, money, and stress when critical deadlines arise.

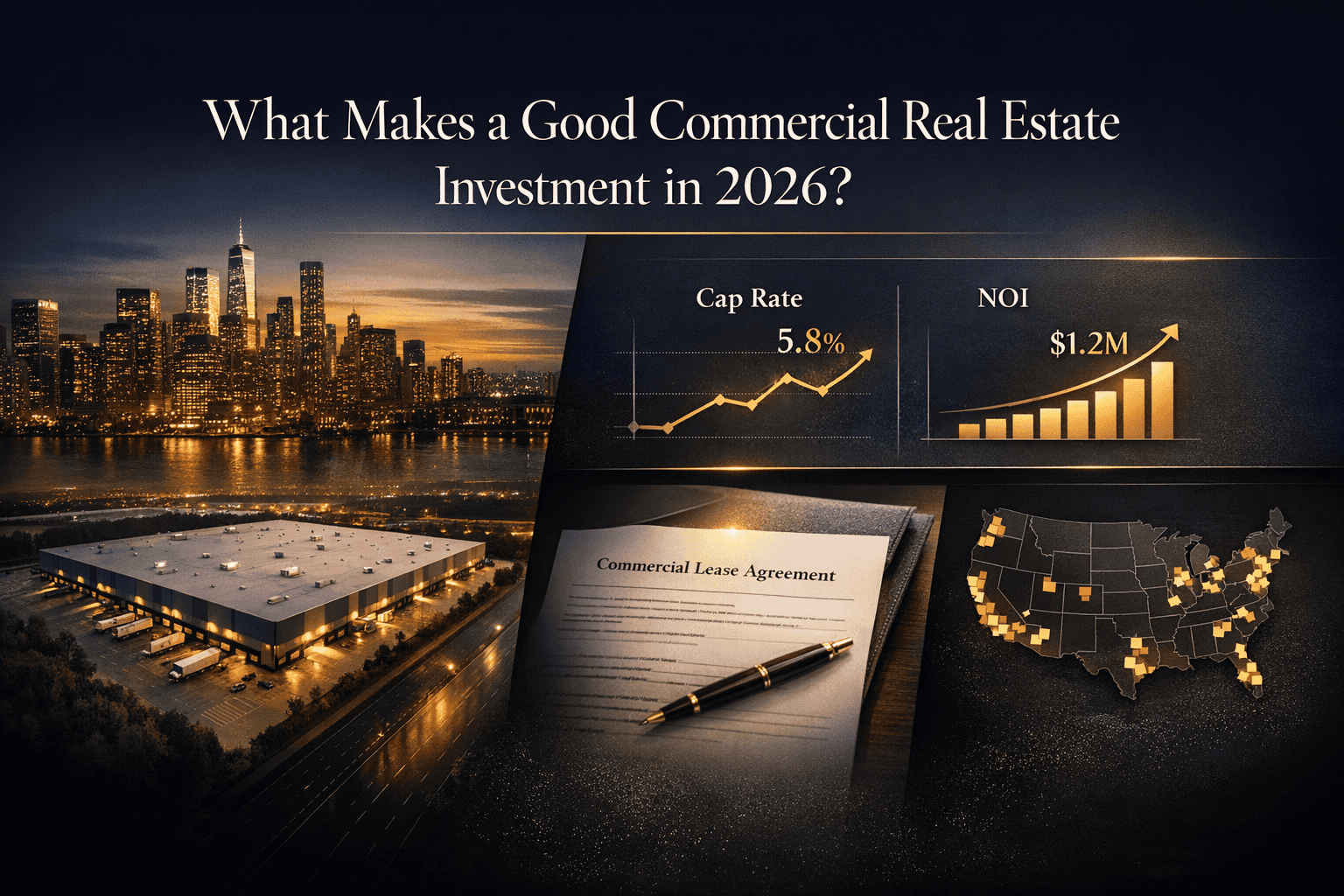

Step 3: Identify and Evaluate the Property

Once your goals are set and your team is in place, it's time to find the right asset. Commercial real estate opportunities come through a variety of channels, including on-market listings, off-market deals, broker relationships, and direct outreach campaigns.

When evaluating a potential property, focus on these key metrics:

- Net Operating Income (NOI): Annual revenue minus operating expenses, excluding debt service.

- Capitalization Rate (Cap Rate): NOI divided by purchase price, used to assess valuation relative to the market.

- Cash-on-Cash Return: Annual pre-tax cash flow divided by total equity invested.

- Debt Service Coverage Ratio (DSCR): NOI divided by annual debt payments — lenders typically require a minimum of 1.25x.

- Vacancy Rate and Tenant Mix: Quality and stability of existing leases and tenant credit profiles.

A thorough financial analysis will help you determine whether the asking price is justified and what your realistic returns might look like under various scenarios. For a deeper look at evaluating asset performance, explore our guide on commercial real estate investment analysis.

Step 4: Submit a Letter of Intent (LOI)

Once you've identified a promising property and completed preliminary underwriting, the next step is submitting a Letter of Intent (LOI). This non-binding document outlines the key terms you're proposing for the transaction, including:

- Purchase price

- Earnest money deposit amount

- Due diligence period length

- Contingencies (financing, inspection, etc.)

- Proposed closing timeline

While the LOI is generally non-binding, it sets the tone for negotiations and establishes mutual expectations between buyer and seller. Work closely with your broker and attorney to craft an LOI that is competitive yet protects your interests.

Step 5: Negotiate the Purchase and Sale Agreement (PSA)

After both parties agree on the LOI terms, your attorney will draft or review the Purchase and Sale Agreement (PSA) — the legally binding contract that governs the transaction. Key provisions to negotiate include:

- Representations and Warranties: Seller disclosures about the property's condition, title, and financial performance.

- Due Diligence Period: The window of time (typically 30–60 days) during which you can inspect the property and review documents without penalty.

- Earnest Money Terms: When deposits become non-refundable and under what circumstances they are returned.

- Closing Conditions: Specific requirements that must be met before the transaction can close.

- Assignment Rights: Whether you can assign the contract to an entity or partner before closing.

Your attorney's expertise is critical here. Even minor contractual oversights can lead to significant financial exposure down the line.

Step 6: Conduct Thorough Due Diligence

The due diligence phase is arguably the most important stage of any commercial real estate deal. This is your opportunity to verify everything the seller has represented and uncover any issues that could affect the property's value or your investment thesis.

Physical Due Diligence

- Property condition assessment (PCA) by a licensed inspector

- Roof, HVAC, plumbing, electrical, and structural reviews

- Environmental Phase I (and Phase II if necessary) assessments

- Survey and boundary verification

Financial Due Diligence

- Review of rent rolls, lease agreements, and tenant estoppels

- Analysis of historical operating statements (typically 2–3 years)

- Verification of property tax history and upcoming reassessments

- Review of CAM reconciliations and expense pass-throughs

Legal and Title Due Diligence

- Title search and review of any encumbrances, easements, or liens

- Zoning verification and compliance review

- Review of existing loan documents if assuming debt

- Confirmation of any pending litigation involving the property

If significant issues surface during due diligence, you may renegotiate the purchase price, request seller credits, or — if the issues are material enough — terminate the agreement within your contingency window.

Step 7: Secure Financing

Unless you're purchasing a property with all cash, arranging financing is a critical parallel process to due diligence. Commercial real estate loans differ significantly from residential mortgages, so understanding your options is essential.

Common commercial financing structures include:

- Conventional Commercial Mortgage: Offered by banks and credit unions, typically requiring 25–35% down and strong DSCR.

- SBA 504 Loan: Ideal for owner-occupied commercial properties with as little as 10% down.

- CMBS Loan (Commercial Mortgage-Backed Securities): Fixed-rate loans typically used for larger income-producing properties.

- Bridge Loan: Short-term financing for value-add or transitional properties not yet stabilized.

- Mezzanine Financing: Subordinate debt used to fill the gap between senior debt and equity.

Lenders will scrutinize the property's financials, your net worth and liquidity, credit history, and experience as a commercial investor. Having a complete and well-organized loan package will accelerate the approval process. Learn more about your options in our overview of commercial real estate financing options.

Step 8: Satisfy Closing Conditions

As the closing date approaches, both buyer and seller must satisfy all conditions outlined in the PSA. For buyers, this typically includes:

- Obtaining a firm loan commitment and satisfying lender requirements

- Ordering and reviewing the title commitment and title insurance policy

- Confirming all due diligence items have been resolved

- Reviewing the closing disclosure and settlement statement

- Wiring the remaining purchase funds to escrow

Your closing attorney or title company will coordinate the execution of all closing documents, including the deed, bill of sale, assignment of leases, and loan documents.

Step 9: Close the Transaction

Closing day represents the culmination of weeks or months of work. On this day, ownership of the property is officially transferred from the seller to the buyer. Key activities include:

- Signing all required legal documents

- Funding the transaction through the escrow or closing agent

- Recording the deed with the appropriate county or municipality

- Receiving keys, tenant contacts, and property management documentation

Once the deed is recorded, you are officially the owner of the property. Congratulations — but the work doesn't stop here.

Step 10: Post-Closing Asset Management

Successful commercial real estate investing doesn't end at the closing table. Effective asset management is what ultimately drives returns over the hold period. Post-closing priorities include:

- Transitioning property management (in-house or third-party)

- Communicating with existing tenants and establishing relationships

- Executing any planned capital improvements or repositioning strategies

- Setting up accounting systems and investor reporting if applicable

- Monitoring lease expirations and beginning renewal or re-leasing efforts early

Your long-term success hinges on how well you manage and optimize the asset after acquisition. Many investors underestimate the operational complexity of commercial real estate — having the right property management team in place from day one is critical.

Common Mistakes to Avoid When Structuring a Commercial Real Estate Deal

Even experienced investors make missteps. Here are some of the most common pitfalls to watch out for:

- Underestimating due diligence: Rushing through inspections or financial reviews to meet an artificial deadline can expose you to costly surprises after closing.

- Over-leveraging: Taking on too much debt can leave your investment vulnerable during market downturns or periods of elevated vacancy.

- Ignoring market fundamentals: Even a great deal can perform poorly in a declining submarket. Always analyze supply, demand, and economic drivers at the local level.

- Skipping title insurance: Title issues can surface years after closing — title insurance protects your ownership rights.

- Poor lease review: Understanding every clause in a lease — especially rent escalations, co-tenancy clauses, and termination rights — is essential to accurately projecting income.

Why Work With Cordura for Your Next Commercial Real Estate Deal?

At Cordura, we specialize in helping investors and buyers across the US market navigate the full spectrum of commercial real estate transactions — from initial property search to post-closing asset management. Our team brings deep market knowledge, a robust network of industry professionals, and a data-driven approach to every engagement.

Whether you're structuring your first commercial deal or expanding a sophisticated portfolio, we provide the expertise and resources to help you achieve your investment goals. Explore our available listings and investment opportunities by visiting our commercial properties for sale page.

Final Thoughts

Structuring a commercial real estate deal from start to finish requires discipline, expertise, and the right team. By following a systematic process — from defining your investment objectives and conducting rigorous due diligence to securing favorable financing and managing the asset post-closing — you can significantly improve your chances of a successful outcome.

The commercial real estate market is full of opportunity for investors who take a strategic, informed approach. With Cordura as your partner, you'll have the guidance and support you need at every stage of the journey.