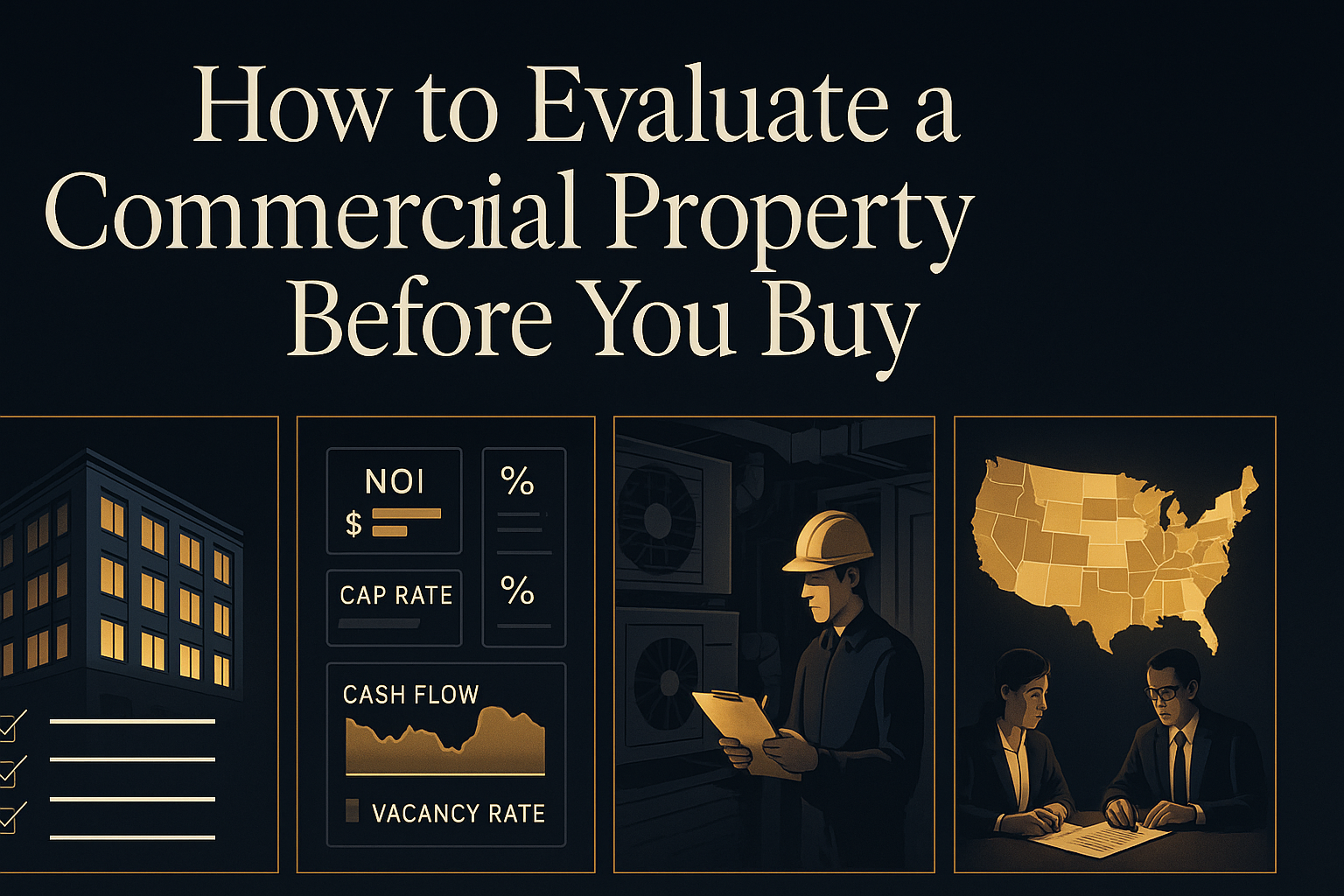

How to Evaluate a Commercial Property Before You Buy

Purchasing commercial real estate is one of the most significant financial decisions an investor can make. Whether you're acquiring an office building, retail strip center, industrial warehouse, or multifamily complex, a thorough evaluation process is essential to protect your capital and maximize your returns. At Cordura, we help investors navigate every step of this process — and it all starts with knowing what to look for before you sign on the dotted line.

This guide walks you through the key pillars of commercial property evaluation, from financial analysis to physical inspections, so you can make confident, data-driven decisions in the US market.

1. Start With Location Analysis

The old adage "location, location, location" holds especially true in commercial real estate. A property's location directly impacts tenant demand, lease rates, vacancy risk, and long-term appreciation potential. Before diving into financials, assess the following location factors:

- Market and submarket conditions: Is the area experiencing population growth, job creation, and economic expansion? Strong fundamentals drive demand for commercial space.

- Accessibility and visibility: For retail and office properties, foot traffic, parking availability, and proximity to highways or transit hubs are critical.

- Proximity to competitors and anchor tenants: Nearby complementary businesses can boost traffic; too many direct competitors may cannibalize your tenant base.

- Zoning and land use regulations: Confirm the property is zoned appropriately for your intended use and investigate any pending rezoning proposals in the area.

Evaluating local market trends requires deep knowledge of the submarket. Explore our commercial real estate market analysis resources to get current data on vacancy rates, absorption, and rental trends across US markets.

2. Analyze the Financial Performance

No evaluation is complete without a rigorous review of the property's financials. This is where you separate a good deal from a great one — or discover red flags before committing capital.

Net Operating Income (NOI)

The NOI is the cornerstone of commercial property valuation. It equals gross rental income minus operating expenses (excluding debt service and taxes). A healthy, growing NOI signals a strong asset; declining NOI warrants deeper investigation.

Capitalization Rate (Cap Rate)

The cap rate is calculated by dividing NOI by the purchase price. It reflects the property's unlevered yield and allows for apples-to-apples comparisons across assets. Lower cap rates typically indicate lower risk and higher demand markets; higher cap rates suggest higher risk or value-add potential.

Cash-on-Cash Return

This metric measures annual pre-tax cash flow relative to the total cash invested. It accounts for debt service and gives a more realistic picture of your actual return on equity in the first year.

Gross Rent Multiplier (GRM)

The GRM is a quick screening tool: divide the purchase price by the annual gross rent. While not a substitute for deeper analysis, it helps you quickly benchmark a property against comparable assets.

Review the Rent Roll

Request a current rent roll listing all tenants, lease terms, rent amounts, escalations, and lease expiration dates. Look for near-term lease expirations that could introduce vacancy risk and evaluate tenant credit quality — a property anchored by investment-grade tenants commands a premium for good reason.

3. Conduct a Thorough Physical Inspection

Even the strongest financials can be undermined by deferred maintenance, structural issues, or environmental liabilities. A comprehensive physical due diligence process should include:

- Structural and envelope inspection: Engage a licensed commercial property inspector or structural engineer to assess the roof, foundation, exterior walls, windows, and parking lots.

- Mechanical, electrical, and plumbing (MEP) systems: HVAC systems, electrical panels, plumbing infrastructure, and elevators all represent significant capital expenditure items if they are aging or underperforming.

- ADA compliance: Verify that the property meets Americans with Disabilities Act requirements — non-compliance can create legal liability and costly retrofits.

- Environmental assessment (Phase I ESA): A Phase I Environmental Site Assessment is standard practice for commercial acquisitions. It identifies recognized environmental conditions (RECs) such as underground storage tanks, soil contamination, or hazardous materials.

- Capital expenditure reserves: Build a realistic CapEx schedule for the next 5–10 years based on the physical inspection findings. This directly affects your underwriting and negotiating position.

4. Review Leases and Legal Documents

Commercial leases are complex legal instruments that govern the economic relationship between you and your tenants. Before closing, have a qualified real estate attorney review all leases and identify:

- Lease type: Is this a gross lease, modified gross, net, double-net, or triple-net (NNN) structure? The lease type determines who bears operating cost risk.

- Rent escalations: Look for annual bumps tied to CPI or fixed percentages — these protect your income against inflation.

- Tenant improvement allowances and free rent: Understand any outstanding landlord obligations to current tenants.

- Options to renew, expand, or terminate: Tenant options can be favorable or unfavorable depending on market conditions at the time they are exercised.

- Co-tenancy clauses: Common in retail leases, these can allow tenants to reduce rent or terminate if an anchor tenant leaves.

- Assignment and subletting rights: Understand if tenants have the right to transfer their lease without your consent.

5. Evaluate the Financing Landscape

How you finance a commercial property affects your returns, cash flow, and risk profile. Key financing considerations include:

- Loan-to-Value (LTV) ratio: Most commercial lenders require 65–80% LTV, meaning you need a meaningful equity contribution. Your down payment directly impacts cash-on-cash returns.

- Debt Service Coverage Ratio (DSCR): Lenders typically require a DSCR of 1.20x or higher, meaning the NOI must cover debt payments with a 20% cushion.

- Interest rate environment: Rising rates compress returns and reduce purchasing power. Model multiple rate scenarios in your underwriting.

- Loan term and amortization: A 10-year fixed-rate loan with 25-year amortization is common for stabilized assets; bridge loans suit value-add plays with shorter business plan horizons.

Understanding commercial real estate financing options available in today's market can help you structure deals that maximize yield while managing risk.

6. Assess Value-Add and Exit Strategy Potential

Sophisticated investors don't just evaluate a property as it is — they evaluate what it can become. When assessing upside potential, consider:

- Below-market rents: If current leases are rolling at rents below prevailing market rates, there's an opportunity to capture upside upon renewal or re-leasing.

- Physical improvements: Lobby renovations, parking lot upgrades, or modernized common areas can justify rent premiums and attract higher-quality tenants.

- Occupancy upside: Acquiring a partially vacant property at a distressed price and leasing it up is a classic value-add strategy — but only works if the market fundamentals support absorption.

- Repositioning or redevelopment: Some properties have highest-and-best-use potential that exceeds their current use. Explore whether zoning allows for denser development or conversion to a higher-value asset class.

Defining your exit strategy before you buy is just as important as the entry underwriting. Whether you plan to hold for income, execute a value-add business plan and sell, or pursue a 1031 exchange, your exit drives the investment thesis.

7. Benchmark Against Comparable Sales

Valuation in commercial real estate is ultimately grounded in what the market will bear. Request a broker opinion of value or commission a formal appraisal, and independently review comparable sales ("comps") for similar properties in the submarket. Evaluate comps on a per-square-foot and per-unit basis, and analyze cap rate trends over the prior 12–24 months to understand whether the market is compressing or expanding.

If you're working with a Cordura advisor, they can provide proprietary comp data and market intelligence to ensure you're paying a fair price — or better yet, identifying a true below-market opportunity.

8. Perform a Sensitivity Analysis

No investment performs exactly as modeled. Build a sensitivity analysis that stress-tests your underwriting assumptions across a range of scenarios:

- What happens to returns if vacancy increases by 10–15%?

- How do returns change if you can't achieve projected rent growth?

- What is your break-even occupancy — the minimum occupancy needed to cover all expenses and debt service?

- How does your IRR change if the exit cap rate is 50–100 basis points higher than you projected?

Investors who stress-test their models are far better prepared for market disruptions and can underwrite with greater conviction. Learn more about investment property due diligence best practices to sharpen your analytical framework.

Final Thoughts: Due Diligence Is Your Greatest Risk Management Tool

Evaluating a commercial property before you buy is not a single step — it's a multi-layered process that combines quantitative financial analysis, hands-on physical inspection, legal review, and market intelligence. Skipping steps in this process is where investors get hurt.

At Cordura, we believe that informed buyers are empowered buyers. Our team of commercial real estate professionals is here to help you source, evaluate, and acquire properties that align with your investment goals — whether you're a first-time commercial buyer or an experienced portfolio builder looking to scale.

Ready to take the next step? Contact the Cordura team today to connect with an advisor who can guide your commercial property evaluation from start to finish.