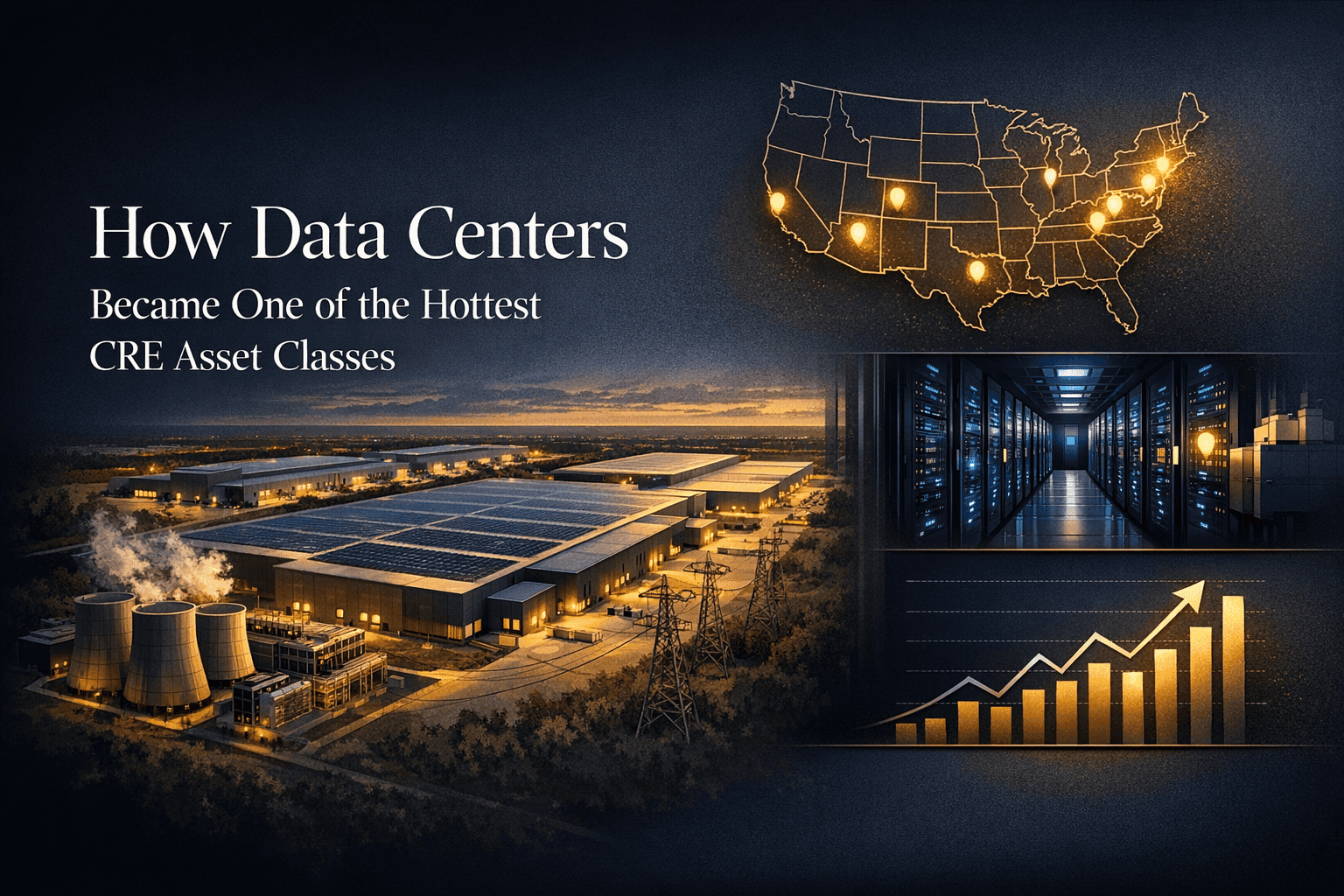

How Data Centers Became One of the Hottest CRE Asset Classes

Over the past decade, commercial real estate investors have watched a quiet revolution unfold in the industrial sector. Data centers — once considered niche infrastructure assets reserved for tech giants — have rapidly emerged as one of the most sought-after asset classes in the entire CRE landscape. Driven by explosive demand for cloud computing, artificial intelligence, and digital connectivity, data center real estate is rewriting the rules of what it means to invest in commercial property.

For investors navigating today's shifting market, understanding why data centers have climbed to the top of the CRE food chain is not just interesting — it's essential. At Cordura, we help investors identify opportunities across every major asset class, including the rapidly expanding world of industrial real estate where data centers are carving out their own powerful niche.

The Digital Economy's Physical Backbone

It's easy to think of the internet as something intangible — a cloud floating somewhere in the ether. But the reality is decidedly physical. Every stream you watch, every email you send, every AI query you submit runs through a vast network of servers housed in massive, highly engineered buildings. Those buildings are data centers, and they represent billions of dollars in real estate investment.

The numbers tell a compelling story. Global data center construction spending surpassed $40 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) exceeding 10% through 2030. In the United States alone, markets like Northern Virginia, Dallas, Chicago, Phoenix, and Atlanta have seen land prices and lease rates skyrocket as hyperscale operators and colocation providers race to secure capacity.

Key Demand Drivers Fueling the Data Center Boom

- Cloud Computing Expansion: AWS, Microsoft Azure, and Google Cloud continue to build out infrastructure at a breathtaking pace to meet enterprise demand.

- Artificial Intelligence Workloads: AI model training requires enormous computational power, translating directly into demand for high-density data center space.

- 5G Network Rollout: Edge computing deployments tied to 5G infrastructure are creating demand for smaller, distributed data center facilities closer to population centers.

- Streaming and Content Delivery: The global appetite for video content keeps climbing, requiring ever-growing storage and processing capacity.

- Enterprise Digital Transformation: Businesses of every size are migrating workloads to the cloud, creating sustained long-term demand.

What Makes Data Centers Attractive to CRE Investors

Beyond the macro demand story, data centers offer a set of investment characteristics that distinguish them from traditional office, retail, or even conventional industrial assets. Understanding these fundamentals helps explain why institutional capital — from pension funds to sovereign wealth funds — has flooded into this sector.

Long-Term, Triple-Net-Like Leases

Data center leases are typically structured with terms ranging from five to twenty years, often with built-in rent escalations. Tenants — whether hyperscale cloud providers or enterprise colocation users — make significant capital investments in the infrastructure they deploy inside leased space. That investment creates powerful switching costs, making tenant retention rates exceptionally high. For investors accustomed to the volatility of shorter-term office or retail leases, this stability is enormously appealing.

Insulation from Remote Work Trends

While the office sector has struggled to define its post-pandemic identity, data centers face no such existential uncertainty. If anything, the shift to remote work accelerated data center demand — more employees working from home meant more cloud-based collaboration tools, video conferencing, and enterprise software, all of which require robust data center infrastructure. This counter-cyclical quality relative to office has made data centers even more attractive to diversified CRE portfolios.

High Barriers to Entry

Developing a data center is not a simple construction project. Facilities require specialized power infrastructure, redundant cooling systems, advanced physical security, and proximity to reliable fiber connectivity. Permitting, utility negotiations, and entitlement processes can take years. These barriers create significant protection for existing operators and investors, limiting supply and supporting long-term rent growth in constrained markets.

Mission-Critical Tenant Profile

The tenants occupying data center space are not discretionary occupiers. Their operations depend on continuous, uninterrupted access to their infrastructure. This mission-critical dependency means tenants are highly motivated to maintain their leases and keep current on rent obligations, creating credit quality profiles that rival — and often exceed — traditional investment-grade commercial tenants.

Primary vs. Secondary Data Center Markets

Not all data center markets are created equal. Understanding the geography of this asset class is critical for investors evaluating opportunities. The so-called NOVA-DAL-CHI-PHX-ATL corridor — Northern Virginia, Dallas, Chicago, Phoenix, and Atlanta — has long dominated U.S. data center activity, with Northern Virginia's Loudoun County earning the nickname "Data Center Alley" for its unparalleled concentration of hyperscale facilities.

However, land scarcity, power constraints, and water usage concerns in primary markets are pushing developers and investors into secondary and tertiary markets. Cities like Columbus, Indianapolis, Salt Lake City, Reno, and Kansas City are increasingly attracting data center development. For value-focused CRE investors, these emerging markets may offer superior risk-adjusted returns compared to the highly competitive primary hubs. This dynamic mirrors broader patterns visible across commercial real estate investment strategies, where secondary market opportunities often outperform during periods of primary market saturation.

Power Is the New Location

In traditional commercial real estate, the mantra is location, location, location. In data center real estate, power availability may be an even more critical determinant of asset value. A data center without access to affordable, abundant, and reliable power is functionally useless regardless of its geographic advantages. As hyperscale demand has exploded, many primary markets face genuine power grid constraints, with utilities unable to connect new facilities for three to five years in some jurisdictions.

This power scarcity dynamic is reshaping investment thesis construction. Savvy investors are evaluating sites not just on existing power availability but on proximity to renewable energy generation, relationships with local utilities, and regulatory environments that support large-scale power procurement. Markets with access to hydroelectric, solar, or wind power at scale — particularly in the Pacific Northwest and the Mountain West — are gaining strategic appeal.

Data Center Investment Structures: How Investors Participate

One of the most important evolutions in data center real estate has been the broadening of investment access. What was once limited to direct development by well-capitalized tech companies is now available to investors through multiple vehicles.

Data Center REITs

Publicly traded Real Estate Investment Trusts (REITs) specializing in data centers — including Equinix, Digital Realty, and Iron Mountain — provide liquid, dividend-yielding exposure to the asset class. These vehicles allow individual and institutional investors to participate in data center economics without the complexity of direct ownership. Data center REITs have consistently outperformed broader REIT indices over the past decade.

Private Equity and Institutional Funds

Private equity firms including Blackstone, KKR, and Brookfield have made massive bets on data center real estate through direct acquisitions, development joint ventures, and portfolio company ownership. Institutional investors seeking yield in a lower-return environment have allocated heavily to these vehicles, recognizing the long-duration cash flow profiles that data centers offer.

Direct Development and Acquisition

For sophisticated CRE operators and developers, direct participation in data center development represents the highest-risk, highest-reward pathway. Build-to-suit development for hyperscale tenants — where a tenant has pre-committed to a long-term lease before ground is broken — has emerged as a particularly attractive model, blending development upside with leasing certainty.

Sale-Leaseback Transactions

Corporations that own their own data center facilities have increasingly pursued sale-leaseback transactions, monetizing their real estate holdings while retaining operational control through long-term leases. These transactions allow CRE investors to acquire stabilized, mission-critical assets with creditworthy tenants already in place.

Risks and Considerations for Data Center Investors

No asset class is without risk, and data centers are no exception. Investors entering this space should be clear-eyed about the unique challenges involved.

Technological Obsolescence

Data center technology evolves rapidly. Facilities built five to ten years ago may require significant capital expenditure to meet the power density requirements of modern AI and high-performance computing workloads. Investors must factor ongoing capital reinvestment into their return models and evaluate whether existing facilities can be upgraded cost-effectively.

Power and Environmental Scrutiny

Data centers consume enormous amounts of electricity and water. As ESG considerations grow in prominence among institutional investors and regulators, data center operators face increasing pressure to demonstrate sustainability credentials. Facilities in markets where environmental permits are tightening — as seen in parts of Europe and increasingly in some U.S. jurisdictions — face real regulatory risk.

Tenant Concentration Risk

Many hyperscale data centers are single-tenant facilities leased to a handful of dominant cloud providers. While these tenants carry strong credit, their departure or lease non-renewal would create significant vacancy challenges given the specialized nature of the asset. Colocation facilities serving multiple tenants offer better diversification but introduce their own operational complexity.

Capital Intensity

Data center development requires substantially more capital per square foot than conventional industrial or office construction. Mechanical, electrical, and plumbing (MEP) systems, backup power infrastructure, cooling equipment, and security systems represent a disproportionate share of total project cost. This capital intensity requires developers and investors to maintain strong balance sheets and access to multiple financing channels.

The AI Inflection Point: Why Demand is Accelerating

If data center demand was already strong before 2023, the emergence of large-scale artificial intelligence applications has added an entirely new dimension to the demand equation. Training and deploying AI models — particularly large language models like those powering ChatGPT and its competitors — requires GPU clusters that consume power at densities far exceeding traditional enterprise IT workloads.

Where a standard data center rack might consume between 5 and 15 kilowatts of power, AI training facilities are designing for rack densities of 50, 100, or even 200 kilowatts. This transformation is driving a wave of next-generation hyperscale development, with Microsoft, Google, Amazon, and Meta collectively committing hundreds of billions of dollars to AI infrastructure buildout through 2030. Every one of those dollars flows, at least in part, through real estate.

For CRE investors, the AI wave represents both an opportunity and a complexity multiplier. Facilities capable of supporting high-density AI workloads command significant rent premiums over conventional data center space. But building for AI density requires more sophisticated engineering, larger power infrastructure, and more advanced cooling solutions, all of which raise development costs and increase the technical expertise required to execute successfully.

How Cordura Helps Investors Navigate the Data Center Opportunity

At Cordura, we understand that data center real estate sits at the intersection of technological transformation and commercial real estate fundamentals. Whether you're a seasoned institutional investor looking to expand your data center allocation or a CRE operator exploring this asset class for the first time, having the right market intelligence and deal-sourcing capabilities is critical.

Our platform provides comprehensive coverage of commercial property listings and investment opportunities across the United States, including industrial and specialized assets in the fastest-growing data center markets. We connect buyers, investors, and property seekers with the resources they need to make informed, strategic decisions in a market moving at digital speed.

The Outlook: Data Centers in the Decade Ahead

The structural forces driving data center demand — cloud adoption, AI proliferation, 5G expansion, and digital transformation — are not temporary trends. They represent a fundamental and sustained shift in how the global economy operates. Commercial real estate that serves as the physical infrastructure of the digital economy is, in many respects, as essential as the highways and ports that enabled the industrial economy of the twentieth century.

Investors who understand this asset class deeply — who can navigate the power constraints, technological evolution, and capital requirements that define it — are positioned to generate compelling risk-adjusted returns across market cycles. For those still on the sidelines, the data center revolution is not a story about the future. It's happening right now, in real buildings, on real land, generating real income. The question is not whether data centers belong in a diversified CRE portfolio. The question is how much and where.