If you spend any time in commercial real estate, you’ll hear one term constantly: cap rate.

It’s one of the fastest ways to evaluate a deal—but also one of the most misunderstood.

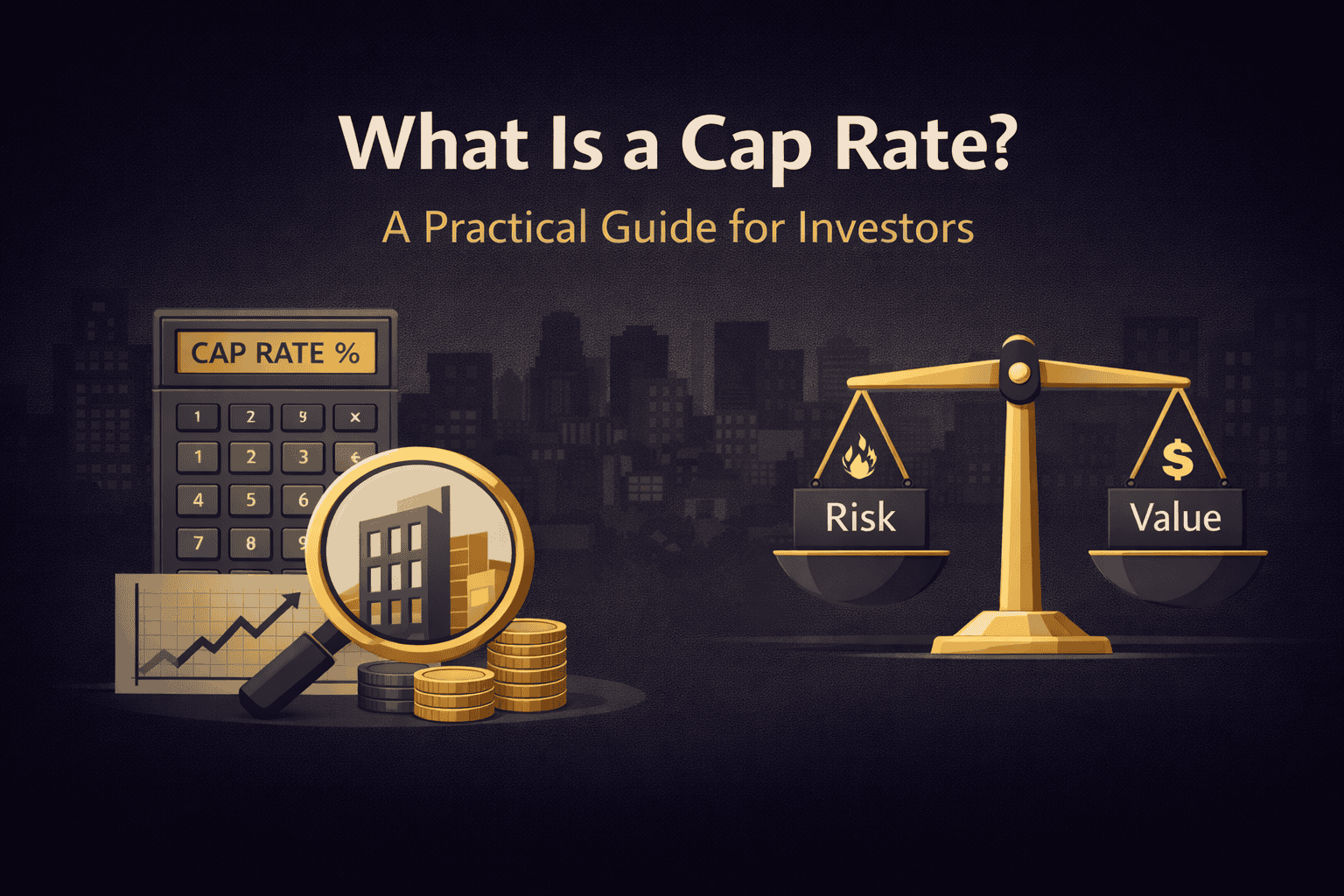

A cap rate isn’t just a percentage. It’s a direct reflection of risk, return, and property value.

What Is a Cap Rate?

Cap rate (short for capitalization rate) is the rate of return a property generates based on its income.

Simple definition:

Cap Rate = Net Operating Income (NOI) ÷ Property Value

It tells investors how much return they’re getting relative to the purchase price.

How to Calculate Cap Rate

The formula is straightforward, but the interpretation is where most people get it wrong.

Example:

-

Net Operating Income (NOI): $100,000

-

Property Price: $1,250,000

Cap Rate = 8%

This means the property is generating an 8% annual return before financing.

What Cap Rate Actually Tells You

Cap rate is not just about returns—it reflects risk and market perception.

-

Higher cap rate ? higher return, higher risk

-

Lower cap rate ? lower return, lower risk

Example:

-

A stabilized property in a prime area ? 5–6% cap

-

A value-add or secondary market deal ? 7–9% cap

Understanding this difference is critical when comparing opportunities.

How Cap Rate Affects Property Value

This is where things get interesting.

Cap rate directly impacts commercial property valuation in Kansas City.

Example:

-

NOI: $100,000

-

At 8% cap ? Value = $1.25M

-

At 6% cap ? Value = $1.67M

Same income—completely different value.

That’s why small changes in cap rate can significantly impact pricing.

Cap Rate vs Cash Flow (Don’t Confuse Them)

A common mistake is assuming cap rate equals actual return.

It doesn’t.

Cap rate:

-

Ignores financing

-

Based on property performance only

Cash flow:

-

Includes loan payments

-

Reflects actual money in your pocket

You need both to fully understand a deal.

What Impacts Cap Rates

Cap rates are influenced by multiple factors:

-

Location and market strength

-

Interest rates

-

Tenant quality and lease terms

-

Property condition

-

Supply and demand

When interest rates rise, cap rates often increase—which pushes property values down.

When to Use Cap Rate (and When Not To)

Cap rate works best for:

-

Stabilized income-producing properties

-

Quick deal comparisons

-

Market benchmarking

It’s less useful for:

-

Development deals

-

Heavy value-add projects

-

Properties with unstable income

Common Mistakes Investors Make

-

Using projected NOI instead of actual

-

Ignoring expenses

-

Comparing properties in different markets

-

Assuming lower cap rate always means better deal

A low cap rate in the wrong deal can still lose money.

How Cordura Helps You Analyze Cap Rates

At Cordura, we don’t just look at cap rates—we break down what’s behind them.

Our approach includes:

-

Accurate NOI analysis

-

Market cap rate benchmarking

-

Deal comparison across asset types

-

Identifying value-add opportunities

Because a number alone doesn’t tell the full story.

Final Thoughts

Cap rate is one of the most powerful tools in commercial real estate—but only if you understand how to use it.

The best investors don’t just calculate cap rates.

They interpret them, challenge them, and use them to find opportunity.

Looking at a Deal?

If you want help analyzing a property or understanding its real return, reach out to our Kansas City investment analysis team—or browse our current commercial real estate opportunities.